Forging an Innovative Oncology Future Post-Biosimilar Era

Executive Summary / Key Takeaways

- Coherus BioSciences has completed a significant strategic transformation, divesting its biosimilar businesses to focus exclusively on innovative oncology, anchored by its differentiated PD-1 inhibitor, LOQTORZI.

- LOQTORZI, the only FDA-approved treatment for nasopharyngeal carcinoma (NPC), is positioned for substantial growth, projected to reach $150 million to $200 million in annual revenue in this indication alone over the next three years, providing non-dilutive funding for the pipeline.

- The company’s pipeline features promising, differentiated mid-stage immuno-oncology candidates, Casdozokitug (anti-IL-27) and CHS-114 (anti-CCR8), with early clinical data supporting their mechanisms and potential in large markets like HCC and solid tumors, with key data readouts expected in the first half of 2026.

- Recent financial maneuvers, including the UDENYCA divestiture and debt paydowns, have significantly strengthened the balance sheet, resulting in a projected $250 million post-close cash balance and extending the cash runway beyond two years into 2027.

- While facing intense competition from larger pharmaceutical companies and inherent clinical development risks, Coherus aims to leverage its differentiated technology, focused commercial capabilities, and strategic partnerships to drive value creation.

201420162018202020222024−200M−100M0100M−200M−100M0100MOperating Cash Flow (USD)Free Cash Flow (USD)Operating Cash Flow (USD)Free Cash Flow (USD)AnnualQuarterlyOperating Cash Flow (USD)Free Cash Flow (USD)

A Strategic Pivot Towards Oncology Innovation

Coherus BioSciences has undergone a profound strategic transformation, shedding its identity as a diversified biosimilar player to emerge as a focused, commercial-stage innovative oncology company. This pivot, culminating in the divestiture of its biosimilar assets, including the significant UDENYCA franchise in April 2025, is not merely a change in portfolio but a fundamental shift aimed at unlocking value through differentiated cancer therapies. The company’s journey from a biosimilar pioneer to an oncology innovator reflects a deliberate strategy to leverage its expertise in complex biologics development and commercialization within a market segment offering potentially higher growth and margin profiles.

The biopharmaceutical industry landscape is intensely competitive, characterized by rapid technological advancement and significant investment in oncology. Large, established players like Amgen (AMGN), Pfizer (PFE), AbbVie (ABBV), and Sandoz (SDZ) command substantial market share across various therapeutic areas, including biosimilars and innovative oncology. These competitors possess significantly greater financial, R&D, manufacturing, and commercial resources. However, Coherus aims to carve out its niche by focusing on potentially best-in-class assets and strategic combinations, rather than competing head-to-head across broad portfolios. The company’s strategic response to this competitive environment centers on leveraging its differentiated technology and focused execution.

The Technological Foundation: Differentiated Assets

At the heart of Coherus’ innovative oncology strategy lies its foundational asset, LOQTORZI (toripalimab-tpzi), a next-generation PD-1 inhibitor. Unlike many existing PD-1 antibodies, LOQTORZI is designed to block PD-1 interactions by binding to the FG loop on the PD-1 receptor. This unique binding epitope is believed to result in differential and potentially superior signaling within the T cell, clinically manifesting in efficacy irrespective of PD-L1 status in certain studies. This differentiation is critical in a crowded PD-1 market dominated by products like Merck’s (MRK) Keytruda and Bristol-Myers Squibb’s (BMY) Opdivo. For investors, this technological nuance translates into a potential competitive advantage, particularly in combination therapies and patient populations less responsive to current PD-1 inhibitors.

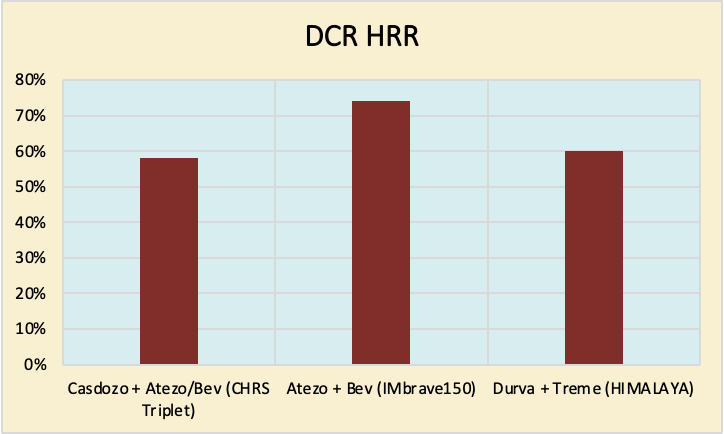

Beyond LOQTORZI, Coherus’ pipeline features two mid-stage clinical candidates targeting the tumor microenvironment (TME): Casdozokitug (CHS-388), an anti-IL-27 antibody, and CHS-114, an anti-CCR8 antibody. Casdozokitug is a first-in-class IL-27 antagonist. IL-27 is an immune regulatory cytokine often overexpressed in certain cancers, contributing to immune suppression. Blocking IL-27 aims to rebalance the TME and enhance anti-tumor immunity. Early clinical data for Casdozokitug in combination with atezolizumab and bevacizumab in first-line hepatocellular carcinoma (HCC) has shown compelling results, including a 17% complete response (CR) rate in a Phase 2 study. This compares favorably to CR rates of 3% and 8% reported in pivotal Phase 3 studies for existing standard-of-care regimens (IMbrave150 and HIMALAYA), suggesting a potential for improved outcomes in a large market with significant unmet need.

CHS-114 targets CCR8, a chemokine receptor highly expressed on regulatory T cells (Tregs) within the TME. Tregs suppress anti-tumor immune responses, contributing to resistance to therapies like PD-1 inhibitors. CHS-114 is designed as a cytolytic antibody to selectively deplete these tumor-resident Tregs. Coherus emphasizes the high selectivity of CHS-114, noting that profiling of some competitor CCR8 antibodies revealed off-target binding with potential toxicity implications. Recent Phase 1 data presented at AACR showed visually compelling biomarker evidence of CHS-114-mediated Treg depletion and subsequent CD8+ T cell infiltration into the tumor, establishing proof of mechanism. This translational data, coupled with an observed partial response in a heavily pretreated, PD-1 refractory head and neck cancer patient, supports the potential of CHS-114 to turn “cold” tumors “hot” and synergize with other immunotherapies. The strategic intent behind these pipeline assets is to develop novel combination therapies with LOQTORZI, addressing mechanisms of resistance and expanding the addressable patient population beyond those currently benefiting from PD-1 monotherapy.

Strategic Execution and Commercial Momentum

The strategic pivot was executed through a series of divestitures. Following the sales of the CIMERLI ophthalmology franchise in March 2024 and the YUSIMRY immunology franchise in June 2024, the UDENYCA divestiture in April 2025 marked the completion of the exit from the biosimilar business. This move was driven by the need to strengthen the balance sheet and focus resources on the innovative oncology pipeline.

LOQTORZI’s commercial launch in the U.S. in January 2024 is central to the new strategy. In the first quarter of 2025, LOQTORZI generated $7.3 million in net revenue, a significant increase from $2.0 million in Q1 2024, reflecting a nearly 269% growth rate. Patient demand grew 15% quarter-over-quarter, driven by new patient starts and increasing duration of treatment. The company’s commercial team is focused on increasing market penetration in the NPC indication, leveraging strong NCCN guidelines that designate LOQTORZI as the only preferred Category 1 first-line treatment option in combination with chemotherapy. While NPC is a rare cancer, requiring a steady ramp-up period, management projects annual LOQTORZI revenue from this indication to reach $150 million to $200 million over the next three years. Achieving quarterly revenues above $15 million is expected to cover commercial costs and contribute to R&D, underscoring LOQTORZI’s role as a funding engine for the pipeline.

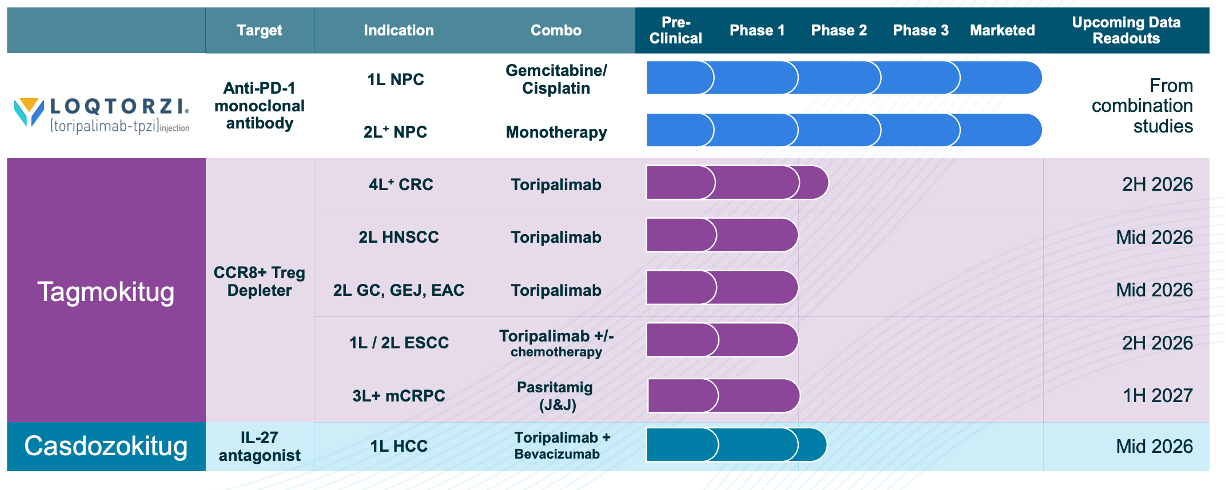

The pipeline development strategy leverages LOQTORZI as a backbone for combination therapies. Internally, Coherus is advancing Casdozokitug and CHS-114 in combination with LOQTORZI in tumor types with strong biological rationale, such as HCC, NSCLC, head and neck squamous cell carcinoma (HNSCC), and gastric cancer. Externally, the company is pursuing strategic partnerships where other companies fund clinical trials evaluating LOQTORZI in combination with their novel agents. Examples include collaborations with INOVIO (INO) in HPV-positive HNSCC, CRI in ovarian cancer, and Junshi Biosciences with its anti-BTLA antibody in small cell lung cancer. This “elegant and efficient” approach aims to expand LOQTORZI’s label across multiple indications with minimal cost to Coherus, while also setting up future revenue opportunities from proprietary combinations with its own pipeline assets.

Financial Performance and Strengthened Liquidity

Coherus’ financial performance in the first quarter of 2025 reflects the ongoing transition and the early stages of the oncology focus. Net revenue from continuing operations (primarily LOQTORZI) was $7.6 million, a substantial increase from $2.3 million in Q1 2024. Cost of goods sold for continuing operations increased proportionally with LOQTORZI sales, reaching $2.7 million. Research and development expenses from continuing operations decreased to $24.4 million in Q1 2025 from $28.4 million in Q1 2024, primarily due to reduced co-development costs with Junshi, partially offset by increased investment in the internal pipeline (CHS-114 and Casdozokitug). Selling, general, and administrative expenses from continuing operations saw a significant decrease to $26.0 million in Q1 2025 from $40.2 million in Q1 2024, driven by lower headcount and the absence of a prior-year impairment charge. The loss from continuing operations was $45.4 million in Q1 2025, an improvement from the $67.8 million loss in Q1 2024.2014201620182020202220240100M200M300M400M500M−300M−200M−100M0100MRevenue (USD)Net Income (USD)Revenue (USD)Net Income (USD)AnnualQuarterlyRevenue (USD)Net Income (USD)

Results from discontinued operations (biosimilars) show net revenue of $32.1 million in Q1 2025, down from $74.8 million in Q1 2024. This decrease is attributable to the divestitures of CIMERLI and YUSIMRY in 2024 and the impact of UDENYCA supply interruptions from late 2024 that affected Q1 2025 sales. Net income from discontinued operations was $9.2 million in Q1 2025, significantly lower than the $170.9 million reported in Q1 2024, which included a $153.6 million gain on the sale of the CIMERLI franchise.

Liquidity has been significantly bolstered by the UDENYCA divestiture. As of March 31, 2025, cash and cash equivalents stood at $82.4 million. The UDENYCA sale, completed in April 2025, brought in $483.4 million in upfront cash (including inventory value). A portion of these proceeds was used to repurchase approximately $170 million principal amount of 2026 Convertible Notes and buy out the UDENYCA royalty obligation for $47.7 million. Following these transactions, Coherus expects to have approximately $250 million in cash on its balance sheet, extending its cash runway beyond two years into 2027. This improved financial position is critical for funding ongoing clinical trials and advancing the pipeline through key data milestones projected in 2026. Management expects full-year 2025 SG&A from continuing operations to be lower than 2024 ($90 million – $100 million projected), driven by approximately $25 million in annualized headcount savings. R&D expense is expected to be higher in 2025 due to increased pipeline investment.2014201620182020202220240100M200M300M400M500MCash and Cash Equivalents (USD)Cash and Cash Equivalents (USD)AnnualQuarterly2014201620182020202220240100M200M300M400M500MTotal Debt (USD)Total Debt (USD)AnnualQuarterly

Competitive Dynamics and Risks

Coherus faces formidable competition in the innovative oncology space. The market for PD-1 inhibitors is crowded, with established players and new entrants like Penpulimab-kcqx recently approved for NPC. While LOQTORZI’s differentiation and NCCN positioning provide an edge in NPC, expanding into other indications will require competing against numerous approved IO therapies and pipeline candidates from companies with vastly superior resources. Similarly, pipeline assets like Casdozokitug and CHS-114 face competition from other novel IO targets and combination strategies being pursued by large pharmaceutical and biotechnology companies.

Key risks include the inherent uncertainties of clinical development, where promising early data may not translate into success in later-stage or pivotal trials. Regulatory approval is not guaranteed, even with positive data. Manufacturing and supply chain risks, highlighted by the recent UDENYCA interruption, could impact product availability. Intellectual property challenges, including potential infringement claims or the inability to adequately protect its own technology, pose significant threats. Financial risks include the need for future funding beyond the current cash runway, the uncertainty of receiving UDENYCA earnout payments, and potential liabilities under transition service agreements. The company also acknowledges a material weakness in internal controls related to inventory documentation, though remediation efforts are underway. Dependence on a limited number of wholesalers for revenue and the impact of healthcare reform measures, such as the IRA, also present ongoing challenges.

Outlook and Path Forward

Coherus’ outlook is centered on driving LOQTORZI growth in NPC and advancing its innovative pipeline. Management projects continued revenue growth for LOQTORZI, aiming for market leadership in NPC. The focus for the pipeline is on achieving key data readouts in the first half of 2026 for studies evaluating Casdozokitug in first-line HCC (in combination with LOQTORZI and bevacizumab) and CHS-114 in second-line HNSCC and gastric cancer (in combination with LOQTORZI). These readouts are critical catalysts that could validate the potential of these assets and inform future development decisions, including potential pivotal trials.

The strengthened balance sheet provides the necessary runway to reach these milestones. The company’s strategic partnerships are expected to contribute to label expansion for LOQTORZI across various tumor types without significant R&D expenditure from Coherus. While the path forward involves significant execution risk in clinical development and commercialization within a highly competitive market, Coherus believes its focused strategy, differentiated assets, and improved financial position provide a solid foundation for creating long-term value by bringing innovative therapies to cancer patients.

The most compelling investment themes are the ones nobody is talking about yet.

Each issue delivers three emerging themes with concrete catalysts, market data, and specific companies positioned to capture growth.

Get 3 under-the-radar themes every Monday.

Conclusion

Coherus BioSciences has successfully executed a transformative pivot, transitioning from a diversified biosimilar company to a focused innovative oncology entity. Anchored by the differentiated PD-1 inhibitor LOQTORZI and supported by a promising pipeline of TME-targeted antibodies, the company is now positioned to pursue growth in the oncology market. The strategic divestitures have significantly improved the balance sheet, providing crucial funding for pipeline development through key data catalysts expected in 2026. While navigating intense competition and inherent industry risks, Coherus’ ability to leverage its technological differentiation, execute its commercial strategy for LOQTORZI, and advance its pipeline through successful clinical trials will be paramount to realizing its vision of extending cancer patient survival and delivering value to shareholders. The coming quarters, particularly leading up to the projected data readouts in 2026, will be critical in validating the potential of its innovative oncology franchise.

20260408

Coherus Oncology Current and Expected Returns.

One approved drug, LOQTORZI®, and a multi billion dollar pipeline. What are the actual Probabilities of Success, and what are the corresponding valuations.

Apr 07, 2026

Below, I will go over Coherus full cash position, pipeline, and potential as an investment, as well as an investment timeframe for both entry and exit.

Pipeline

While this graphic from their presentation gives a good overview, there are still some caveats I want to discuss here.

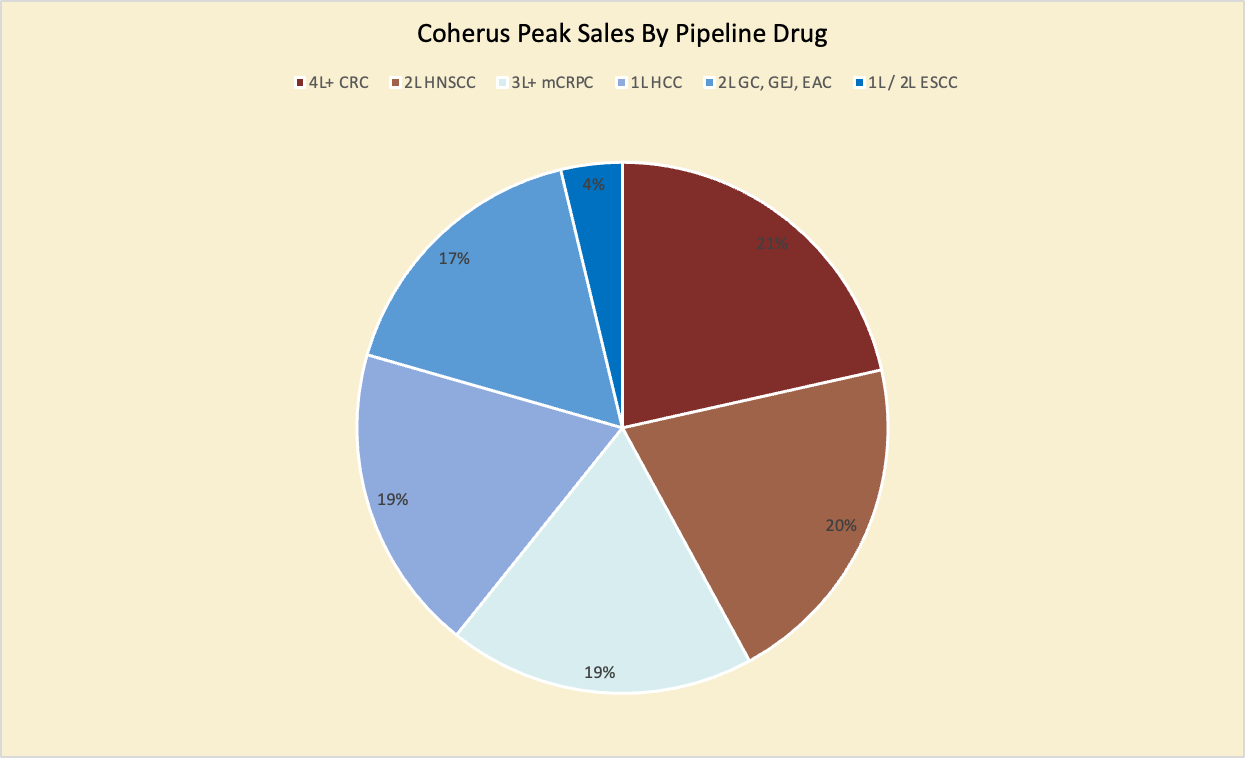

Below you can see the peak-sales distribution, with peak sales as the weight in the total pipeline peak-sales of USD 21.4 B:

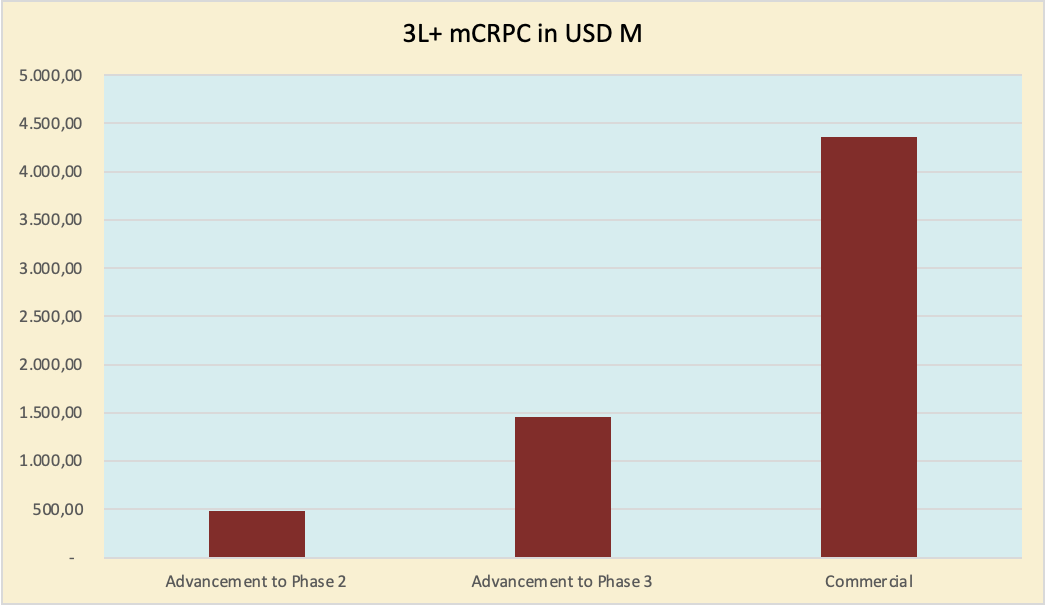

What I find fascinating about Coherus is that its market cap is only USD 261 M. Even a Phase 1-to-2 advancement of one of their three 4 billion+ drugs, which is likely to occur in approximately 80% of cases, since the PoS of advancing from Phase 1 to Phase 2 is about 50%, could significantly boost the market cap.

The graph below shows what the Phase 1-to-2 (and beyond) advancement of one of the Phase 1 drugs with peak sales of 4 billion would look like.

This is not the only case: as you can see in the distribution above, any of the high-peak-sales drugs could completely change Coherus’ market cap.

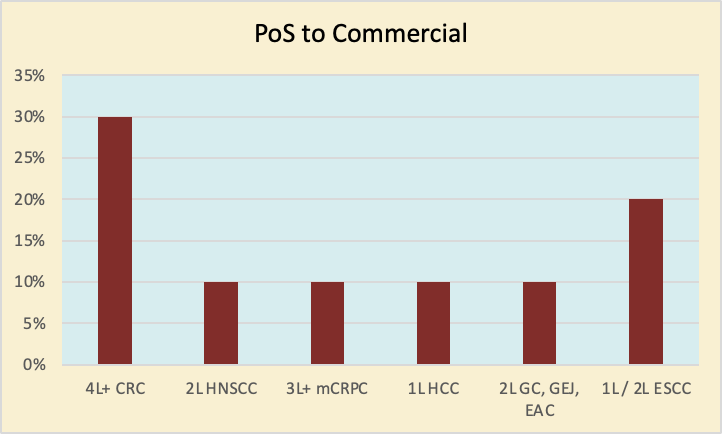

That, for the value, to go over the PoS of every stage and the efficacy of every drug would be too much for this article, but I made a graph showing each pipeline drug’s PoS to commercialisation. I used these numbers for the DCF, and they are on the lower end because I would rather undervalue a company than overvalue it, and I like to invest based on probability-adjusted ROI. In reality, these numbers all could be 5-10% higher.

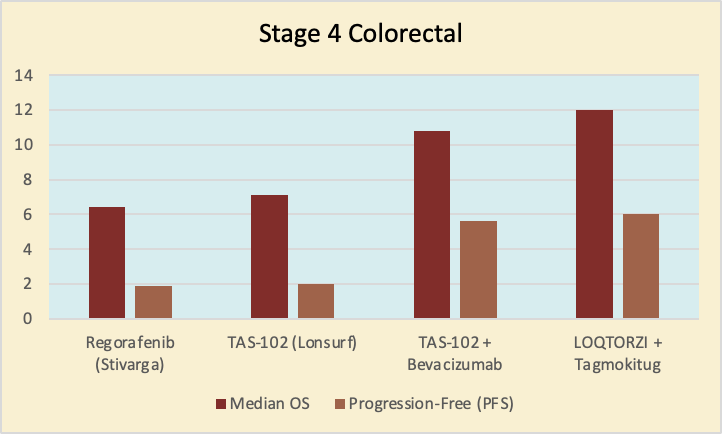

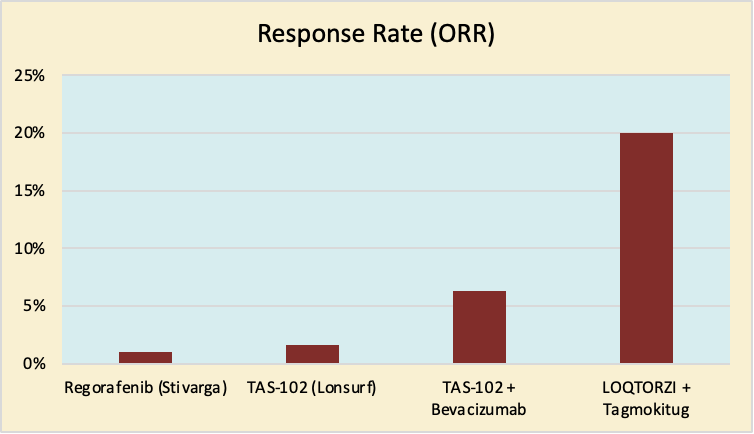

CRC

The article is already too long, and examining every drug like this would completely inflate its length, but I want to examine the two Phase II assets here.

As you can see below, CRC is a double-edged sword for Coherus and should be used in specific situations, given that the OS and PFS are comparably low while the ORR is very high. (peak-sales: USD 750M)

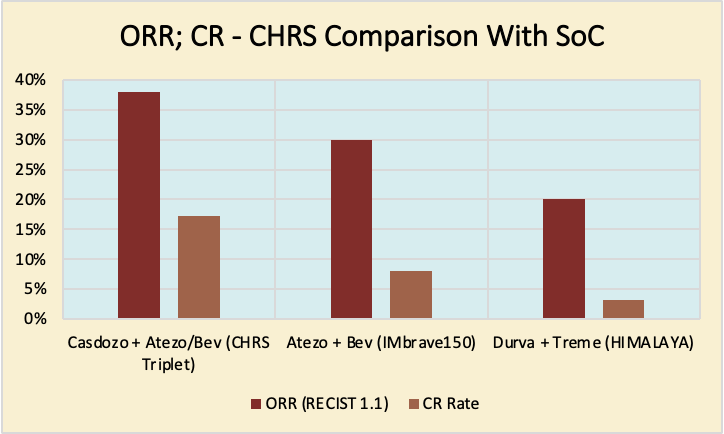

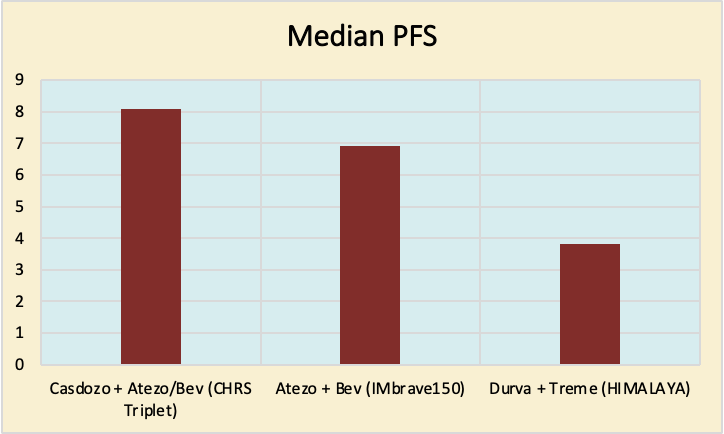

HCC

As CRC is a double-edged sword for Coherus, so is Hepatocellular Carcinoma. At USD 4B peak sales, this drug could have a profound impact on the valuation if it succeeds in Phase II. The drug’s strength lies in the complete control rate, the objective response rate and the progression-free survival. Its weakness lies in the disease control rate. This essentially means their drug Casdo doesn’t stop or slow down as many tumours, but it stops more tumours completely.

Cash Runway

Coherus is technically not just a clinical-stage company, but their only approved drug, LOQTORZI, is not profitable and, if continued at the same projections, will not reach profitability before the marketing expenses for their pipeline drugs are necessary; thus, I would largely value CHRS like a preclinical company.

Their current cash position will bring them through 2026, which is a data-rich year, as in the graphic above.

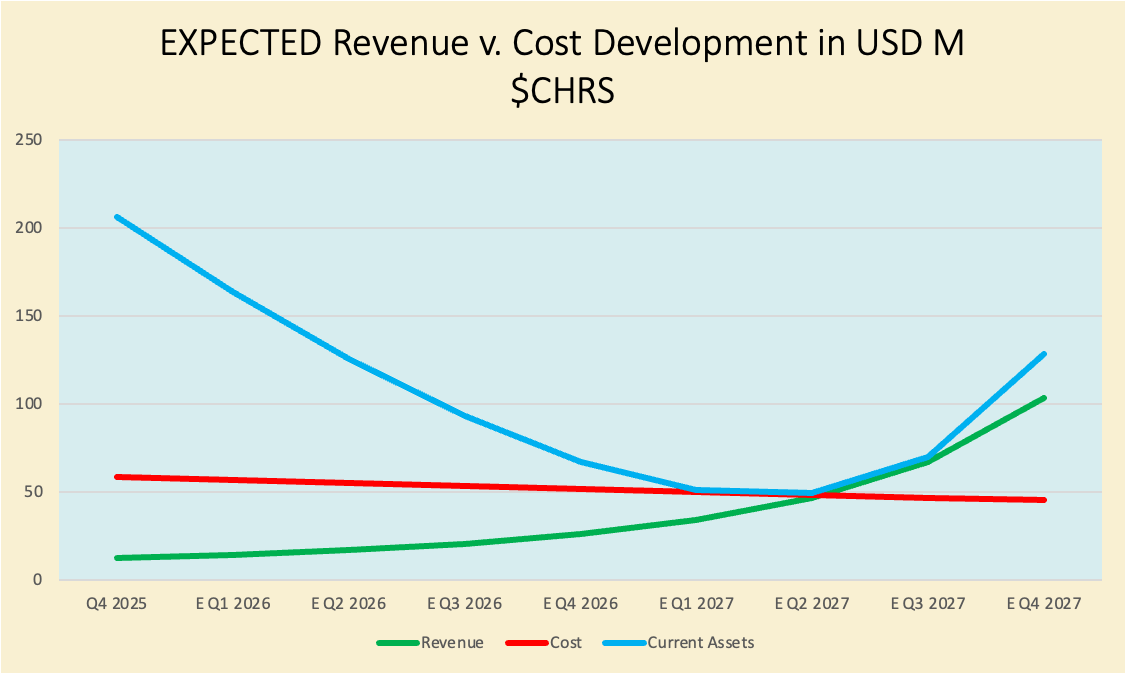

To visualise the situation, I first want to show what Coherus profitability of LOQTORZI’s looks like when isolated:

As you can see in the graph, with 15% YoY revenue growth and 3% annual cost reduction, the company would likely turn profitable without raising much, if any, additional capital.

Part of these cost reductions is due to lower interest rates. In a divestiture, they recently paid off almost all of their debt. They sold their UDENYCA (biosimilar) franchise for USD 558M, which they used to pay off their debt, reducing it from USD 480M to about USD 38.8M as of early 2026.

This is unlikely to happen, but it gives me confidence that in failed trials, the whole company would likely not need to be completely dismantled.

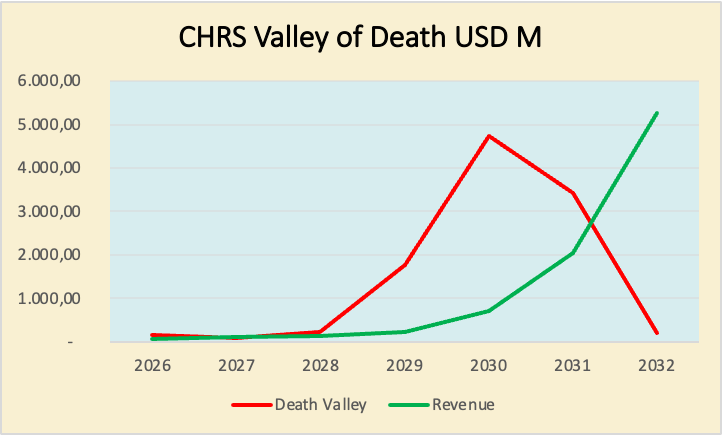

Here is some version of what could actually happen at a much smaller scale, since they are developing a massive pipeline of new drugs, which will sharply increase R&D and M&S expenses in the future. Coherus still has to leap over a huge valley of death. Their pipeline is actually so huge that this valley, compared to their current market cap, looks completely unrealistic.

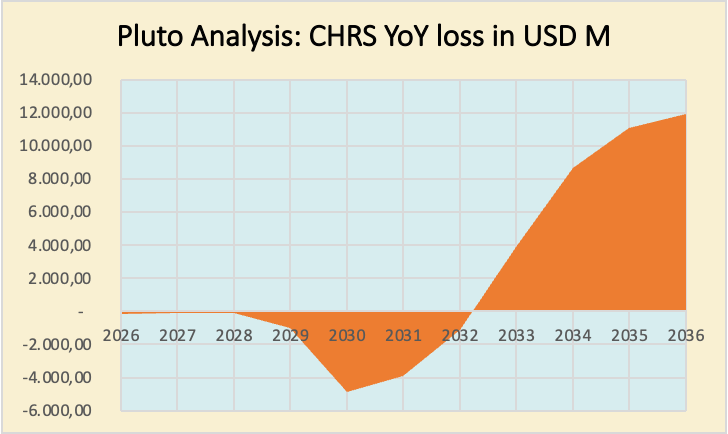

In this graph, the red line shows the yearly loss, while the green line shows the corresponding revenue, which starts to cover losses in 2033.

Since Marketing expenses are usually expected to be 30% of the drug’s peak sales starting the year of marketability, and 3% the year before, we can see a huge spike in expected spending when we enter 2029.

This exact scenario is likely not going to happen, but it paints a picture of the actual costs associated with their drugs and the need for either a massive partnership or outlicensing of some of their pipeline drugs.

Below is another graph of Death Valley, which shows their need for either licensing or an acquisition, and is also prompted by the CEO’s age, which I will discuss later.

Importantly, this does not yet include the necessary total R&D cost, which I will roll out in the valuation section.

Management

I will keep this short. In my Calculations, I use metrics such as outside tasks, public image, and experience to evaluate the quality of the CEO and management on a scale of 0 to 10.

On my scale, Coherus management scores 9,3 which is comparatively high. There are some other items that need to be addressed, though.

- There is some uncertainty about a successor. Yes, the company is young, and yes, there are experienced people at Coherus, but given the CEO’s age and the situation they are in, this needs to be addressed in the valuation.

- The CEO is 70 – this means he is likely looking for retirement, which is especially important considering that they are reaching a discounted valuation peak only in about 9 years, which means there is some time to accumulate.

I found an additional yearly 5% discount due to management risk, adequate for Coherus.

Valuation

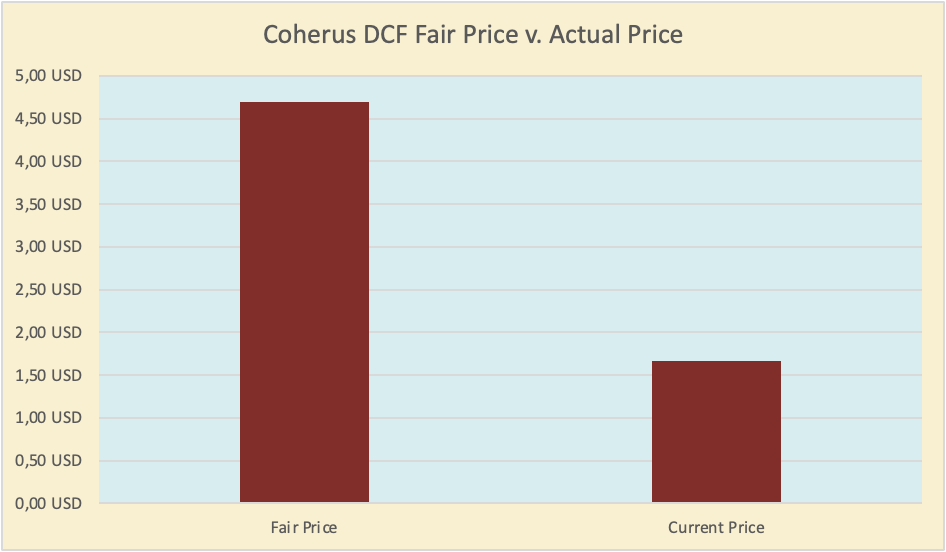

In my DCF, I found that Coherus is currently undervalued:

According to my DCF, a fair value for Coherus’ share price would be 4.70 USD at the current stage, vs. 1.67 USD, the current market price.

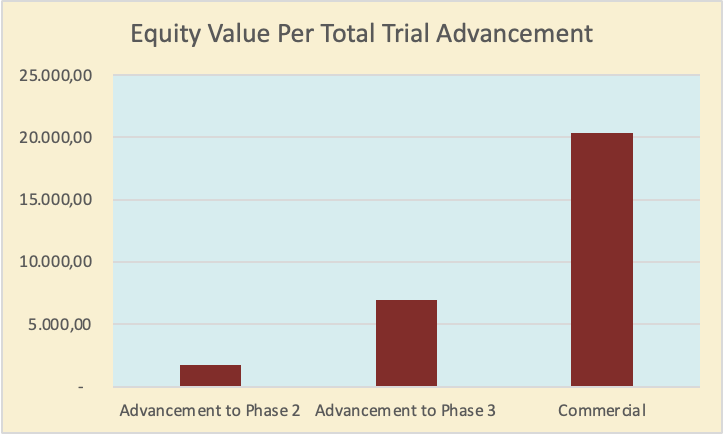

Now, there is some reasoning behind this discrepancy, which has to do with the funding issues I outlined above, as well as their recent divestiture of the biosimilar business. In the best case, they can quickly find a partner to out-license one of their products for Biobucks and Royalties, or they get acquired soon after major Phase II and III advancements. Below, I made a graph outlining potential acquisition prices at their trial stages. This is also in case all their trials are advancing at each stage, as in the other graphs; take this with a grain of salt.

This graph accounts for the current Phase II drugs’ advancement into Phase III, as I have outlined above. Funding this would be incredibly difficult and likely dilute shareholders.

This graph depicts potential acquisition prices for Coherus at each stage.

If Coherus tries to fund these trials itself, it would, if even possible, significantly dilute shareholders.

.

For oncology, to fund their trials, Coherus would likely need to raise USD 10-20M per Phase II trial and USD 50-100M per Phase III trial. Since they are currently conducting four Phase I trials and 2 Phase III trials, the total cost to fund all their trials would likely exceed USD 400 M+. It’s hard to pinpoint exact numbers here, and the new FDA Optimus design doesn’t make this easier.

If they can progress most of their trials, they might be able to raise capital without diluting too heavily.

As you can see, the complete Phase II advancement alone could put the company at around USD 2B in market cap, causing necessary equity raising to fund corresponding trials of about USD 40M (Avg. cost), which would keep dilution under control at this stage when it comes to R&D. For the total Phase III advancement Avg. cost per trial is at USD 50-100M, so 6 x 100M on the high end, also because of the new FDA trial design, we would get USD 600M in cost, which could mean dilution % = $0.6 Billion / $5.6 Billion → Dilution % = 0.1071, or 10.71%.

Now, even though these are cumulative across all trials, we can use these numbers to estimate the average dilution cost per Phase II trial at 2-5% and per Phase III trial at 10%, while commercialisation might cut as high as 20-40%, depending on the amount of drugs and peak-sales commercialised.

Expected ROI

In the face of the graph above, the buyout value would be the multiple of the market cap at trial advancement above, minus dilution and plus premium.

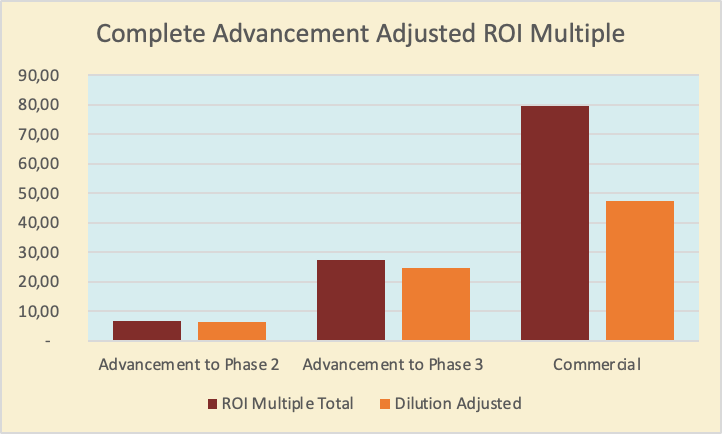

Below, I have plotted the potential multiple on your investment if all trials advance at each stage, next to the dilution. In this graph, you can clearly see why finding a licensing partner or an acquisition might be very beneficial to avoid the heavy Phase III marketing dilution.

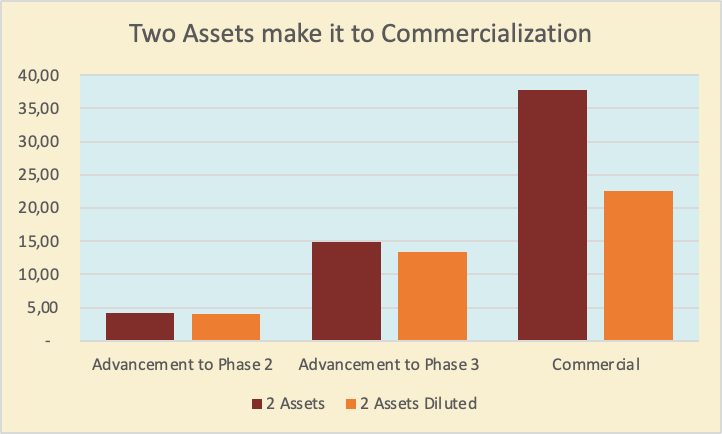

Below, I plotted a similar scenario in the case of only 2 drugs advancing. This is more likely than the above scenario at about 60-70% due to the sheer amount of drugs in their pipeline.

Something I really like about Coherus is that even in a complete trial failure, there is at least some valuation floor because of LOQTORZI.

Now I value this investment more than other Biotech investments. Coherus has incredible strengths, but also some weaknesses, like the CEO. In my quality-, dilution- and time-adjusted multiple, Coherus is valued at 3.4x its current value. This is largely due to a revenue peak occurring 9 years ago, discounted at my personal WACC, the PoS and the Management discount I discussed above.

This multiple is especially important if you have a diversified Biotech portfolio, since Biotech is time-dependent.

Key Risks

- Trial Failure. Failing a trial is very likely. Coherus has shown promising data, but trial design can still fail, and sometimes using a larger sample size can change study outcomes.

- Dilution. Even in trial successes, dilution is likely and always a risk, especially at the current market cap.

- Competition. Oncology is a competitive sector. If Coherus enters the commercial stage, there is always the risk that a competitor will launch a better product, which would hurt Coherus’ outlook.

Entry

In light of the current geopolitical situation, especially the ultimatum to Iran, I would wait at least until the deadline (tonight at 8 pm) before entering the stock market. I think the event will be bipolar only downward in the short run, with the upside coming further in the future, since there will be no quick end to the shortage of oil, as well as the whole international landscape moving toward closer ties with Iran, as for example, India looking for an oil deal. Any downturn in the stock market can significantly increase your ROI, especially given this market cap.

Further, since the CEO has undershot expectations for their LOQTORZI sales, non-profitable biotech companies are usually negatively affected by 10-Qs. Another strategy would be to wait until their 10-Q release, then enter a position.

Exit

As I depicted above, when exiting, I would consider the dilution probability. This also depends heavily on how many drugs they can retain in their pipeline, with more drugs requiring more dilution, since LOQTORZI could pay for a larger share of the required capital if they have fewer drugs to commercialise. Although a USD 175M may not make a huge difference when you need USD 1B+ for marketing.

In case of a buyout in Phase II, this question is redundant.

Conclusion

Should you buy Coherus? CHRS is a strong buy if you have a Biotech or growth portfolio that is well-diversified. The potential returns are really high, and the downside is buffered by LOQTORZI.

If you are not diversified, do not buy Coherus, as trials can fail; for example, the chance of a Phase I trial advancing to the commercial stage is about 10%.

I give Coherus a Pluto Value (I created it, so I will name it) of 3.4x, which is close to its DCF fair value at a share price of USD 4.7.

Enter after the deadline tonight, or after earnings, or in two instalments.

If you read until here, you are exactly what this account is for. Please consider the following.