Contrary to popular belief, the shorts who profited on this drawdown shouldn’t be seen as evil. They identified an opportunity and executed well. Despite the effect that had on our long positions, they played it correctly. They read the technical setup, recognized the breakdown, positioned accordingly, and made money. That’s not villainy. That’s competence.

Most shorts aren’t looking to wipe out your account or destroy companies. They’re simply playing both directions to maximize profit opportunity. And while everyone’s focused on today’s bounce, those shorts just covered. The buying pressure we’re seeing? A meaningful portion is shorts taking profits and closing positions. The same people who profited from the decline just became the buyers contributing to the recovery.

Some of the institutions that profited on the way up likely contributed to the decline after systematically distributing near the top. They sold into strength, potentially shorted the breakdown, and now they’re covering into the bounce. They know how to profit in both directions. That’s not manipulation. That’s understanding market structure well enough to position for what’s actually happening rather than what you wish was happening.

This is a lesson you can capitalize on. If you can add two-way trading to your toolkit, drawdowns become opportunities in multiple dimensions. The obvious one is scaling core positions at better prices. But there’s another most retail traders never consider. If you can identify the technical breakdown early enough, you can position for the move down as a hedge. Generate capital during the decline that you can redeploy at lower prices. You’re not abandoning your thesis. You’re using market mechanics to your advantage while the structure resets.

Some institutions that are net long over multi-year timeframes still short tactical breakdowns within that larger position. When they see distribution patterns developing or technical breakdowns, they’ll reduce exposure or even go net short temporarily. Then they use those profits to reload at better prices. This isn’t betraying conviction. It’s operating with the flexibility that actual market conditions demand.

The moral outrage about shorts misses the point. They serve critical functions. They provide liquidity on the way down, which creates the entry points long-term accumulators need. They challenge overextended valuations. And when they cover, they provide buying pressure that contributes to recoveries. Understanding that function is essential to understanding how markets actually work.

You don’t have to become a dedicated short seller. But understanding that shorting is a legitimate strategy rather than an attack changes how you think about market structure. It helps you recognize when you’re on the wrong side of a technical breakdown. It creates optionality in your positioning rather than forcing you to hold and hope through every decline.

The best traders aren’t ideologically committed to being long or short. They’re committed to reading structure correctly and positioning accordingly. That flexibility, that willingness to profit from volatility in both directions rather than just enduring it from one side, is part of what creates edge. The market doesn’t reward loyalty to positions. It rewards correct reading of structure and appropriate positioning.

does this diamond in the rough have the ability to see three figures long term in your opinion?

Unless there is a fundamental change to the core business, I still firmly believe this will be a triple digit stock in the years to come. The infrastructure thesis is too ironclad for me to think otherwise. The capacity constraints are real. The power allocation advantages are tangible. The customer demand isn’t speculative. These aren’t narrative-dependent variables that shift with sentiment. They’re structural realities that take years to replicate and provide genuine competitive moats.

Q1 2026 is when we’ll start seeing it ultimately reflected in the numbers. That’s not a random timeline. That’s when the capacity expansions come online and start generating the revenue that the current valuation doesn’t fully capture. When those earnings hit and the revenue growth becomes undeniable, the gap between current valuation and actual business performance closes dramatically.

The drawdowns we’re seeing now are broad market pullback, sector rotation, sentiment shifts, and technical positioning. None of that affects whether the megawatt capacity gets built, whether the power gets allocated, whether the customers show up. Those things are happening regardless of what the stock does this week or this month.

What would change my mind? Fundamental deterioration. Loss of key contracts. Capacity expansion delays that push the timeline beyond Q1 2026. Competitive dynamics that erode the power allocation advantage. Evidence that customer demand isn’t materializing. None of those things are happening. The business is executing on schedule.

Triple digits isn’t hope or momentum-based prediction. It’s a math problem. If the capacity comes online as planned, if the revenue materializes as the contracts suggest, the business will be generating cash flow that supports a much higher valuation. Q1 2026 is when that math becomes visible to everyone, not just to those doing the forward analysis now. Between now and then, the stock will do whatever it does. That’s just volatility between here and there.

can you summarize what we can expect going forward with the next few weeks and months ?

Honestly, I have no idea what the next few weeks or months will look like for price action. Could go lower. Could bounce and chop. Could grind higher. Short-term price movement is driven by sentiment, sector rotation, technical positioning, and variables I can’t predict with any reliability.

What I’m watching for falls into two categories. Fundamentally, I’d be concerned about capacity expansion delays, loss of key customer contracts, competitive dynamics that erode advantages, or deterioration in the business model.

Technically, I’m watching for signs of structure recovery. Whether we reclaim key levels that were lost during this pullback. Whether volume patterns shift from distribution to accumulation. Whether we see failed breakdown attempts that suggest selling pressure is exhausted. Whether momentum indicators start showing positive divergences. The technical setup will tell me if this was just a shakeout or if there’s more structural damage that needs to heal.

20251117

There are positions you hold quietly. You check them occasionally. You’re comfortable with the thesis. You don’t feel compelled to explain them to anyone. They just sit there doing their job.

Then there are positions you can’t stop talking about.

You explain the thesis to anyone who’ll listen. You post updates. You defend the idea against skeptics. You write detailed analyses. You check the price constantly. You feel the need to validate your conviction publicly, repeatedly, often.

The interesting question isn’t whether this is good or bad. The interesting question is: what does the compulsion to talk about it reveal?

I’ve held APLD since sub-$6. Watched it run to $40. Experienced the volatility. Held through drawdowns. Built detailed analyses of the data center thesis, the megawatt land grab, the structural monopoly that power allocations create in AI infrastructure.

And I can’t stop talking about it. Not to my audience. To myself.

I’ve written more about this position than any other I’ve held. I’ve explained the thesis dozens of times in different ways. I’ve posted updates about price action. I’ve analyzed the megawatt land grab framework repeatedly. I’ve calculated the math on contracted revenue versus market cap more times than necessary. I’ve written about why I’m holding through volatility, why the thesis remains intact, why patience matters.

Here’s what that compulsion reveals about me, specifically.

It reveals I want to make absolutely certain I can hold through whatever comes next. Not because the position is oversized. I’m comfortable with the size. But because I know from experience that conviction erodes under sustained pressure, even when sizing is appropriate. Every time I write about it, I’m reinforcing the framework I’ll need when price action inevitably tests me again. I’m building the psychological scaffolding in advance, not because I need it now, but because I’ll need it later.

It reveals I’m trying to help others see what took me months to understand. When I post about APLD, I’m not looking for validation of the thesis. I’m looking for validation that the effort to explain it matters. I want people to engage, to learn, to benefit from the work I’ve done. That validation fuels my willingness to keep contributing. The compulsion to explain isn’t about needing agreement on whether I’m right. It’s about wanting confirmation that sharing the insights is valuable. And that’s different. I’m not managing my conviction. I’m managing my motivation to keep teaching.

It reveals I’m genuinely fascinated by the gap between what I see and what the market prices. I check price action not because I need validation, but because I’m watching a thesis play out in real time. Every move teaches me something about how markets price structural advantages before they become obvious. The constant monitoring isn’t anxiety. It’s the intellectual curiosity of watching theory become reality, and wanting to understand every step of that process.

It reveals I’m aware of opportunity cost in real time. I can see other opportunities. I watch other positions move while APLD consolidates. The talking is partly about articulating why staying in this position makes sense given what else is available. It’s not anxiety. It’s active portfolio management. Every position has opportunity cost, and constantly explaining why this one is worth the capital allocation is how I stay disciplined about not chasing every shiny object that moves.

Most importantly, it reveals this position has become part of my identity in a way that’s probably unhealthy. I’m not just long APLD. I’m “the APLD guy” to some portion of my audience. My reputation is now tied to whether this thesis plays out. That changes the psychology entirely. I’m not just managing a position. I’m managing a public narrative. And every time I post about it, I’m deepening that entanglement.

That’s what the compulsion to talk reveals when you’re properly positioned and genuinely convicted. It’s not anxiety. It’s intellectual engagement, motivation management, and identity formation around ideas you believe in deeply.

But most people who can’t stop talking about positions aren’t operating from that place. For them, the compulsion reveals something different entirely. And understanding the difference matters.

Now extend this framework to positions where the talking comes from a different place. Where it’s not confidence seeking engagement, but uncertainty seeking validation.

When someone constantly explains their thesis and it feels repetitive, they’re reinforcing their own conviction because underneath, they’re not as certain as they need to be. The talking is the tell. Quiet confidence doesn’t need constant articulation, but manufactured confidence does.

When someone defends a position aggressively and it feels defensive rather than educational, they’re defending their decision to hold, not the thesis itself. If the skeptics are right, that means they should have exited already, and that thought is intolerable. So they argue. Not because argument changes the thesis. Because argument makes them feel more certain.

When someone posts updates more frequently as volatility increases and the tone shifts to reassurance-seeking, that’s anxiety management. They’re seeking confirmation from their audience that holding through pain is brave rather than stupid. They need external validation because their conviction is wavering. The update isn’t information. It’s a request for support disguised as transparency.

When someone sizes a position too large and becomes an evangelist for it, they’re trying to create a community of believers who will hold with them so they don’t have to face drawdowns alone. They’re not trying to help you. They’re trying to help themselves by surrounding themselves with people who reinforce the decision they’ve already made. Misery loves company, but so does overexposure.

When someone can’t stop recalculating the same math, contracted revenue versus market cap, potential upside, risk-reward ratios, they’re not discovering new information. They’re trying to make the numbers soothe their anxiety about whether they’re right or just early or just wrong. The repetition is a coping mechanism. If they believed the math, they’d calculate once and move on.

The positions you can’t stop talking about are the positions that have you, not positions you have.

When you’re properly sized, properly convicted, and properly patient, you don’t feel the need to explain yourself constantly. You check in occasionally. You reaffirm the thesis when something material changes. But you don’t need to write dissertations justifying why you’re still holding. You don’t need social proof. You don’t need validation. You just hold, quietly, because you know what you own and you’re comfortable with the wait.

The talking is diagnostic. It reveals something is misaligned. For anxious holders: position size exceeds psychological capacity, timeframe expectations don’t match reality, or conviction is intellectual rather than operational. For confident holders: identity has become entangled with outcomes, or intellectual fascination has crossed into compulsion.

For me, with APLD, the diagnostic is clear. This position matters to my psychology in a way that goes beyond the numbers. Not because it’s oversized, but because I’ve built so much intellectual scaffolding around it. I’ve spent thousands of hours understanding the thesis, and now I want to make sure that understanding holds under pressure. I’m checking price action more than someone with a three to five year thesis probably should, not out of anxiety, but because I’m genuinely fascinated by how the market prices what I believe is obvious structural advantage.

None of this means selling. It means being honest about what the compulsion reveals. It’s conviction reinforcement through articulation. And that’s fine. As long as you’re not confusing the talking with the thesis.

Because the thesis doesn’t care whether I talk about it. The thesis plays out or it doesn’t based on whether secured power allocations create monopoly renewal pricing in 2027 to 2030, not based on how many times I explain it.

The positions you can’t stop talking about reveal something about where you are psychologically with that position. For some, it reveals weakness, oversizing, conviction gaps, mismatched timeframes. For others, it reveals engagement, intellectual fascination, identity formation around ideas. But it always reveals something diagnostic. And if you’re paying attention, that information is more valuable than whatever the position does next. Because you can use it to adjust, to right-size, to extend timeframes, to detach identity, or simply to accept how you’re wired and position accordingly.

20251120

There’s something unique about watching time validate what you’ve been saying. Last night I barely slept. Not from anxiety, but from the weight of seeing thousands of hours of research prove out in real time. Every quarter that prints, every guidance beat across the infrastructure stack, every new contract signed, it all reinforces the thesis we’ve been building. The bull case isn’t just holding. It’s strengthening with each data point.

I spent hours last night going deeper into the numbers, cross-referencing filings, tracing the connections between enterprise deployments and infrastructure commitments. It might look like obsession from the outside. Maybe it is. But when you see an opportunity this large forming in real time, it’s hard to look away. Despite the volatility, despite prices that feel elevated to most people, we’re still early. That’s not hyperbole. That’s what the data shows when you follow the lock-in mechanisms through each layer.

I know I repeat myself. I know I come back to the same points about switching costs, about contractual obligations, about power allocations that can’t be replicated. But that repetition comes from recognizing what’s actually happening here. This is a once in a lifetime setup. I don’t say that lightly. I’ve lived through opportunities that completely transformed my financial reality. I know what they look like when they’re forming, and I know how rare they are.

That’s why I share this research openly. This isn’t about me winning anymore. I’ve already won. My life changed years ago through positioning ahead of transformative shifts. What drives me now is helping others see what I’m seeing before it becomes obvious to everyone. Because once it’s obvious, the asymmetry is gone. The opportunity to build generational wealth exists in the window before consensus catches up to reality.

I genuinely want people reading this to accumulate wealth that changes not just their lives but their children’s lives. Wealth that creates optionality, that removes financial stress, that lets them focus on what actually matters. That’s not exaggeration or sales pitch. That’s the actual outcome I’m working toward by sharing this analysis.

I built my understanding through pattern recognition, through making mistakes and learning from them, through thousands of hours of independent research. Nobody handed me a framework. I had to develop it by studying markets, watching how infrastructure buildouts actually work, understanding where the real advantages form. Sharing what I’ve learned isn’t just for my benefit. It’s offering others the shortcuts I wish I’d had when I was figuring this out myself.

If even a handful of people position themselves well because they understood what’s forming, understood why this infrastructure buildout is different, understood the timing window, that’s worth every hour spent researching. This opportunity is real. The data supports it. The mechanisms are defensible. And the window is open right now. That’s why I keep coming back to it. Not because I need validation. Because I want others to benefit from seeing what’s forming before the market fully prices it in.

20251120

Gap closed. The pullback should have been anticipated. They weren’t going to leave it there. (kavastocks)

you’re such a clown. You were so bullish a couple days ago. Hope you lost big for polluting this environment with your bullish nonsense.(xxx)

This is a perfect example of why most people never build wealth. Let me show you exactly what you’re doing wrong.

You’re celebrating other people’s losses because you need to feel validated about not participating. That’s not analysis. That’s toxicity masquerading as skepticism, and it’s the exact mentality that keeps people poor.

Here’s what you’re actually demonstrating: you can’t distinguish between price volatility and fundamental deterioration. The stock moved down, so you think that proves you were right to stay out. It doesn’t. It proves you don’t understand what you’re analyzing.

Nothing about’s APLD fundamental position changed. CoreWeave still has $11 billion in contracted revenue over 15 years. The first 50MW at Polaris Forge 1 is still operational. The power allocations in North Dakota still can’t be replicated by competitors for 5-10 years. The project financing is still secured against contracted cash flows that dwarf the debt.

What changed? Market sentiment. Some participants got nervous about leverage and sold. That’s it. If you think temporary price action validates your skepticism, you’re confusing noise with signal. And that confusion is exactly why you’ll watch from the sidelines while others compound wealth.

Infrastructure assets with contracted revenue are valued on discounted cash flows, not quarterly price movements. The contracts are still there. The cash flows are still coming. The only thing that moved is sentiment about what premium to pay above those contracted cash flows.

This is what separates investors from spectators. Investors buy cash flows at a discount and endure volatility. Spectators watch prices move, celebrate when others face paper losses, and congratulate themselves for not participating. You’re demonstrating the spectator mentality perfectly.

Paper losses mean nothing if the underlying asset is generating contracted cash flows. The stock could go to $10 and it wouldn’t change that Polaris Forge 1 is producing revenue under a 15-year contract. The people who understand that will accumulate at lower prices. The people who don’t will sell at the bottom and complain when it recovers.

If you’d done the work to understand project financing, you’d know that $2.35 billion in debt secured against $11 billion in contracted revenue isn’t a “debt bomb.” It’s appropriately structured infrastructure financing. Sophisticated institutional lenders underwrote those notes after analyzing the same contracts you’re dismissing. Do you think you know something they don’t? Or is it more likely you’re reacting emotionally to leverage numbers without understanding the structure?

Here’s what’s actually toxic and worth calling out: treating investing like a team sport where you root for others to lose so you feel validated. That mindset ensures you’ll never build real wealth because you’re more interested in being right about short-term price action than understanding what actually drives returns.

The people who succeed separate signal from noise. They don’t confuse volatility with fundamental deterioration. They don’t celebrate paper losses. They focus on whether contracts are being fulfilled and cash flows are materializing.

You’re doing the opposite. You’re focused on short-term price action, emotionally invested in being right about your skepticism, and treating others’ losses as validation rather than asking whether the underlying thesis has actually changed. That’s not analysis. That’s ego protection. And it’s exactly the behavior pattern that keeps most people from building wealth.

If you actually wanted to understand what’s happening, you’d read the CoreWeave contracts. You’d learn how take-or-pay agreements work. You’d study how project financing is structured. You’d understand how power allocations create structural moats that can’t be competed away on relevant timelines.

But you won’t do that work. You’ll keep watching the stock price and celebrating paper losses. And the people who did the work will compound wealth while you spectate. When the facilities are operational and cash flows are printing, you’ll complain that you “knew it all along” but somehow never positioned for it.

That’s the difference. Investors do the work, take positions based on fundamentals, and endure volatility. Spectators watch prices move and congratulate themselves for not participating.

You’re a perfect example of the spectator mentality. And that’s exactly why opportunities like this exist. People like you get shaken out by volatility while people who understand fundamentals accumulate at discounts. The market rewards patience and punishes emotional reactions to noise.

So thank you for providing this teaching moment. You’ve demonstrated exactly what not to do: confusing price volatility with thesis validation, celebrating others’ paper losses to protect your ego, and treating short-term noise as if it’s fundamental analysis.

Keep doing that. Keep celebrating paper losses. Keep confusing volatility with vindication. And keep wondering why the people who did the work end up with the returns while you watched from the sidelines, convinced you were right the whole time.

20251120

Here’s something that doesn’t make sense at first glance.

Hyperscalers have been steadily raising infrastructure spending guidance for months now. Analysts write it up as “hyperscalers betting big on AI.” The stocks move. Everyone debates whether the spending is justified. Standard story.

Except they’re not betting on anything. They already sold that capacity.

Not in some abstract “we think demand will come” way. They actually sold it to enterprises who’ve already embedded AI into production systems serving real customers right now. Hyperscalers didn’t sign 15-year infrastructure contracts and then hope to fill them. They signed because they’ve already committed that capacity downstream to companies who can’t easily leave.

That changes everything about how you analyze this.

When you think hyperscalers are the customers, you worry about demand risk. What if AI spending slows down? What if they overbuilt? What if scrutiny forces them to pull back on capex? Those questions make sense if hyperscalers are speculating on future demand. They don’t make sense if hyperscalers are fulfilling obligations to customers who’ve already locked themselves in.

And those customers are locked in harder than most people realize. Not because the technology is so transformative they can’t imagine leaving. Because switching costs compound faster than anyone models. When a company builds their customer service platform on one provider’s AI infrastructure, integrates AI tools into their development workflows, or deploys AI systems across their data analysis operations, they’re not using commodity services they can swap out next quarter. They’ve integrated APIs, trained employees, built workflows, and connected systems that all depend on those specific implementations. Moving means rebuilding from scratch, retraining teams, risking downtime, and testing everything again to make sure it works. Most companies won’t do that unless something breaks catastrophically.

So you’ve got three layers of lock-in, each reinforcing the others.

Layer one is enterprises. They’re embedding AI into production systems right now. Not pilots. Not experiments. Production systems that serve customers, automate workflows, and generate revenue. Customer service platforms handling thousands of interactions daily. Development tools that entire engineering teams depend on. Data analysis systems that inform business decisions across departments. These aren’t optional nice-to-haves you turn off when budgets tighten. These are operational infrastructure that businesses run on. And every month they operate, switching costs accumulate. More integrations. More trained employees. More dependent systems. More reasons not to move.

Layer two is hyperscalers. They’re locked in through downstream commitments to those enterprises. When a hyperscaler signs a 15-year data center contract, they’re not speculating that demand might materialize. They’ve already sold that capacity forward to enterprises who can’t easily leave. The hyperscaler can’t slow down infrastructure spending because their customers won’t let them. Those customers have production systems running. They have SLAs to meet. They have growth plans that assume capacity will be available. Hyperscalers aren’t building infrastructure on faith. They’re building it because they’ve already committed it downstream.

Layer three is data center operators. They control power allocations that took years to secure and can’t be replicated on relevant timelines. When hyperscalers need capacity now because enterprises are already demanding it, they don’t have the luxury of waiting five years for competing infrastructure to come online. They sign long-term contracts with whoever has power available. And those operators who moved early now have multi-year head starts that competitors can’t close because the constraints are regulatory approval cycles and grid capacity, not capital or technology.

That’s not three separate bets. That’s a chain where each link reinforces the others. The faster enterprises adopt AI, the faster hyperscalers commit to infrastructure. The more infrastructure commitments hyperscalers make, the more contracts get signed with data center operators. And the more those contracts get signed, the harder it becomes for anyone to pull back because the obligations cascade through every layer.

And here’s what most people miss: the window where companies can easily switch providers is closing fast.

Right now, some enterprises are still evaluating. Testing different providers. Comparing capabilities. But every month that passes, more production systems go live. More dependencies get created. More switching costs accumulate. Once a company has spent six months integrating AI into operations, training teams, building proprietary systems on top of a provider’s infrastructure, the activation energy required to switch becomes enormous. Not impossible. Just expensive and risky enough that almost nobody bothers unless forced.

That’s the race nobody’s talking about. Not who builds the best models or who has the most compute. Who captures enterprises before those switching costs solidify. Hyperscalers aren’t just selling AI capabilities. They’re racing to become the infrastructure layer that enterprises can’t afford to leave. Because once they secure that position, they’re not competing for customers anymore. They’re collecting rent on infrastructure those customers depend on.

And data center operators at the bottom of this stack aren’t exposed to demand risk in the way most people assume. They’re not betting enterprises keep spending on AI forever. They’re positioned at the foundation of a compounding lock-in mechanism. Enterprises lock into hyperscalers. Hyperscalers lock into infrastructure. Infrastructure locks into power that can’t be replicated. Each layer makes the others more defensible.

But there’s something deeper happening here that changes the entire risk analysis.

Most infrastructure markets eventually normalize through competition. New entrants see high returns, capital floods in, supply catches up, margins compress. That’s the standard cycle. It works because three conditions hold: capital can replicate the advantage, time to build is faster than market growth, and customers can switch when better alternatives emerge. None of those conditions hold here.

Capital can’t replicate power allocations because regulatory approvals take five to ten years. You can’t throw money at permitting, environmental review, and grid interconnection timelines. Time to build infrastructure is slower than enterprise lock-in formation. By the time a competitor brings capacity online, the enterprises they hoped to serve have already embedded themselves into existing providers. And customers can’t easily switch because switching costs compound monthly. After 18 months of operation, the cost of switching isn’t just migration expenses. It’s organizational disruption, retraining overhead, system testing, and the risk that something breaks in production.

That’s a specific breakdown of competitive dynamics where the normal corrective mechanisms fail. In most markets, high margins attract competition, competition adds supply, supply moderates pricing. The cycle self-corrects. But that cycle requires customers to be able to switch when alternatives arrive. If they can’t because they’re locked in, new supply doesn’t correct anything. It just sits idle while existing suppliers extract rent from customers who have no realistic exit.

This creates a fundamentally different risk profile. Traditional demand risk has fat left tails because customers can leave quickly if they want to. Structural lock-in has thin left tails because enterprises can’t easily leave even if they wanted to, which means hyperscalers can’t pull back even if scrutiny mounts, which means infrastructure spending is defensible even through economic cycles. The lock-in mechanism converts demand volatility into contractual obligations that persist regardless of sentiment.

The bear case everyone’s worried about assumes hyperscalers are building speculatively and will pull back when scrutiny mounts. But they’re fulfilling obligations to enterprises who’ve already embedded AI into operations and aren’t ripping out production systems because someone decides valuations are too high. They’re staying because switching costs compound every month and alternatives aren’t meaningfully better.

Data center operators with secured power aren’t betting on AI adoption continuing. They’re benefiting from lock-in that’s already forming at every layer above them. Enterprises can’t easily leave hyperscalers. Hyperscalers can’t easily stop building infrastructure. Infrastructure providers can’t easily be replaced because power allocations are scarce and alternatives take years to develop. That’s a structural position that gets stronger as the lock-in compounds.

And here’s the timing element most people are missing. This lock-in is forming right now, in 2025, as enterprises move from pilots to production deployments. It’s not obvious yet to most investors because the lock-in happens gradually, one integration at a time. In 18 to 24 months, it will be obvious. Enough time will have passed that even skeptics can see enterprises aren’t migrating away. By then, valuations will have adjusted to reflect the defensibility.

If you’re waiting for more proof before positioning, you’re missing that the lock-in is forming right now, and by the time it’s obvious to everyone, the opportunity is gone.

20251121

Nothing has changed except the number on the screen.

Once you realize that, the more liberated you’ll feel. The business is executing. The contracts are intact. The infrastructure is being built. The only thing that changed is what the market decided to pay for it today versus last week.

Price action is not the same as thesis deterioration. When fundamentals remain solid and the stock pulls back, that creates opportunity. The same business at a lower price is better value, not higher risk. But the market doesn’t always price things rationally in the short term. Sentiment shifts. Participants get nervous. Selling happens.

That’s when conviction gets tested. Anyone can hold when stocks go up. The real question is whether you can hold when they go down for reasons that have nothing to do with the underlying business. If you understood why you bought, and those reasons haven’t changed, then the pullback is noise.

I see this as a buying opportunity setting up, and smart money does too.

But here’s what matters most: do what’s right for your psychological profile. If the volatility is causing you stress, your position size is wrong regardless of whether the thesis is correct. If you can’t sleep, you’re sized too large. If watching drawdowns makes you want to sell at the bottom, you need to reduce exposure.

There’s no shame in that. Position sizing for your actual psychology is more important than being intellectually right about a thesis.

Some people can hold through 50% drawdowns without blinking because they trust their analysis and have long time horizons. Other people can’t, and that’s fine. Know which one you are and act accordingly.

The thesis didn’t break. The price moved. Those are different things.

Smart money understands that distinction. Nervous money doesn’t. Figure out which one you are, then buy, hold, or sell based on that self-knowledge rather than based on what the screen shows you today.

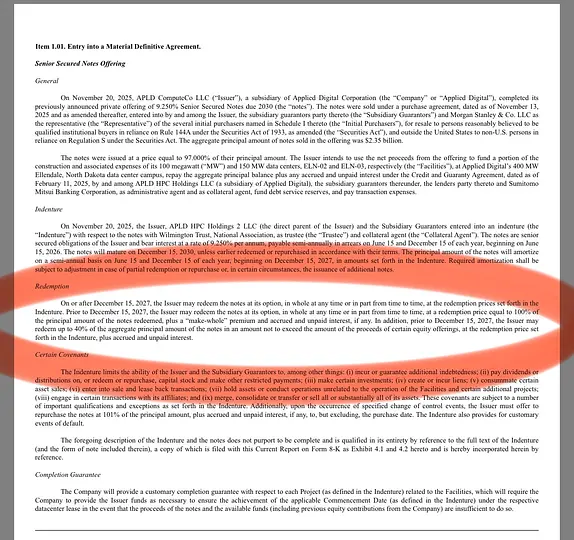

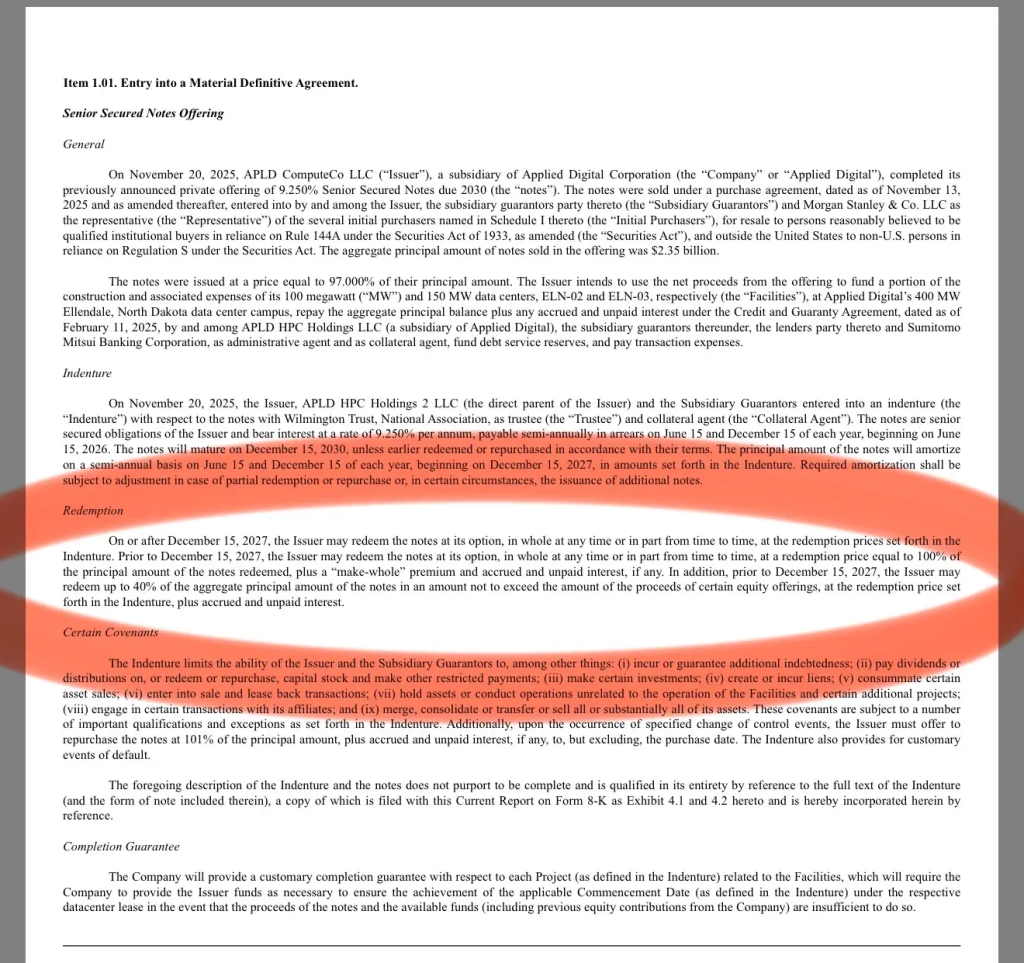

you’re pretty much right about everything but in order to be objective, you need to highlight on $2.3B convertible note offering as well to rationalize the current price action. This is one thing definitely changed.

The redemption clause on Form 8K says APLD can pay off up to 40% of $2.3b by shares prior to Dec 2027. It means they can dilute anytime for around $1B dollar equivalent shares, god knows at what price. They know, their friends know, whether it is $10, $15 or $20. That’s why big fishes and their friends are selling. People think no dilution but if you read this form 8k, you will know it. Plus people think all the money for construction but 8k says only a portion will go to construction. Again market understands all this indirect dilution and stuff. Well they did a few bad things so we suffer for now.

Let’s be honest for now, so everything is on the table. FYI – I am holding big long position.

You’re misreading the redemption terms.

The company can’t force dilution before December 2027. The redemption clause you’re referencing works the opposite way: APLD has the option to call the notes for cash after December 2027, not force conversion at bad prices before then.

The conversion price is set at $9.75 with a 32.5% premium. The capped calls at $14.72 limit dilution on the upside. The company already bought back $84M in shares to offset the potential dilution from conversion.

The concern about “dilution at any price they want” doesn’t match how convertible notes work. Noteholders convert when it’s profitable for them to convert, not when the company decides. If the stock is below $9.75, they don’t convert. If it’s above $9.75, the capped calls protect against dilution up to $14.72.

This is standard convertible financing for infrastructure buildout. The selloff is sentiment around leverage and sector rotation, not some hidden dilution mechanism. The notes were disclosed transparently in public filings. There’s no conspiracy where “big fishes and their friends” are selling based on secret knowledge.

If you’re concerned about the capital structure, that’s fair. But the specific dilution mechanics you’re describing aren’t accurate based on the actual terms.

Wonderful. My initial thought was $20 conversion price but with recent price action, i was pretty sure it will be around $10 but now you confirmed under $10, glad my assumption was right.

Form 8k disclosure is always a high level summary, the devil is always in the details (good or bad). Since you referenced to conversion price and other details, i would appreciate if you can share something that i can take a read into. I like to be correct, not to argue for argument sake. One is sure that all along i was right about convertible option for $2.3B and low conversion price. Anyway, if you share snapshot of the doc, i will take a read and share with you my thoughts. I always try to be objective regardless of my position. Thanks

Thanks for sharing. I will look into it but at a first glance, one thing came to my attention that on PR they say they may not redeem before Dec 1 2027 ….whereas on 8K they said the issuer may redeem 40% prio to Dec 2027, which is a huge contradiction …take a comparative read

We’re looking at two completely different bond offerings here, which is why it seems contradictory.

The Convertible Notes from last year ($450M):

These are the ones I was talking about in my original comment. They have the $9.75 conversion price and $14.72 capped calls. The company can’t touch these before December 1, 2027 – no redemption, no forced conversion, nothing. The press releases about these are from October/November 2024.

The Senior Secured Notes from this week ($2.35B):

These are brand new – just closed November 20th. Completely different instrument. These are straight debt (not convertible), 9.25% coupon, and yes, APLD can redeem up to 40% of these with equity proceeds before December 15, 2027. This is what you’re seeing in that 8-K.

So there’s no contradiction – they’re just two separate bonds with their own terms. The dilution mechanics I explained in my original post apply to the convertibles. Those haven’t changed. The 40% equity redemption thing is for the new senior secured notes that have nothing to do with conversion or dilution concerns.

20251126

Everyone knows data centers need power. That’s obvious. What’s not obvious is why North Dakota’s combination of power infrastructure and climate creates advantages that can’t be replicated on any timeline that matters for investment positioning.

The power dynamics are the foundation. But they’re reinforced by climate advantages that reduce costs, regulatory support that accelerates development, and infrastructure that eliminates constraints limiting growth elsewhere. Each advantage compounds the others. Together they create a moat that gets wider over time.

Start with what makes North Dakota different on power. The state generates more electricity than it consumes. About 42,000 gigawatt-hours annually, but only uses two-thirds of it. Nearly a third of power generated gets exported to other states and Canada. This isn’t a state dealing with capacity constraints. This is a state with surplus generation actively looking for customers.

The generation mix matters. 54% coal provides stable baseload. 35% wind provides cheap renewable energy. 7% natural gas ramps for peak demand. 5% hydro fills gaps. When other regions are straining their grids and watching costs rise, North Dakota has headroom and competitive rates. That’s the foundation.

But here’s where it gets interesting. North Dakota has 4,500 megawatts of installed wind capacity with more coming online. The problem is transmission. Those wind farms produce more power than the transmission lines can move to other markets. The utilities are paying for power they can’t sell, and that cost gets passed to ratepayers.

Data centers solve this problem. Applied’s facilities sit near wind farms that lack sufficient transmission to export production. By consuming power on-site, Montana-Dakota Utilities offset customer costs by roughly$2.0 million in a single year. The data center isn’t competing for scarce power. It’s absorbing surplus that would otherwise be curtailed or sold at terrible prices.

This creates a relationship where incentives align. Data centers provide stable, high-volume demand that maximizes infrastructure utilization. Utilities don’t need to build expensive transmission to export power. They sell locally at attractive rates while improving economics. That’s why North Dakota utilities court data center development instead of fighting it. They actually want this.

The regulatory environment accelerates everything. Light regulation on resource use. Fast permitting. A state government treating data centers as economic development rather than burden. The North Dakota Transmission Authority explicitly identifies data centers as opportunities to monetize energy resources. Nobody is creating obstacles. They’re removing them.

Now add climate. North Dakota’s cold temperatures reduce cooling costs that typically eat 30-40% of data center energy consumption. AI workloads generate massive heat. GPU clusters running AI training hit 40-50 kilowatts per rack versus 5-10 kilowatts for traditional servers. That heat has to go somewhere.

When outdoor temperatures stay below freezing much of the year, you use free air cooling instead of mechanical refrigeration. North Dakota averages around 40F annually with winter regularly below zero. When it’s negative 10 outside, you’re not running chillers. You’re just moving air.

The power efficiency compounds. In hot climates you might need 1.5-1.7 megawatts total to deliver 1 megawatt of compute after cooling overhead. In North Dakota that ratio approaches 1.1-1.2 for much of the year. At scale, that difference means 15-20% more compute in the same power envelope. More revenue from identical infrastructure.

Cold climate also extends hardware lifespan. Electronics degrade faster at higher temperatures. Running servers cold means reduced thermal stress, lower failure rates, longer replacement cycles. When you’re operating thousands of GPUs at $30,000+ each, hardware longevity isn’t trivial. The savings accumulate over years.

The supporting infrastructure reinforces these advantages. Adequate water resources without scarcity concerns. Low natural disaster risk – no hurricanes, earthquakes, wildfires, or flooding at scale. Cheap land enabling large facilities with expansion room. The state invested in fiber connectivity specifically to attract data centers. None of these alone create a moat, but they eliminate constraints that limit development elsewhere.

Now look at replication. A competitor wanting comparable capacity needs surplus power generation, transmission constraints creating local surplus, favorable utility relationships willing to commit infrastructure, and cold climate enabling efficient cooling. Then you need the supporting factors – water, low disaster risk, land, connectivity. Those conditions don’t exist in many places. Where they do exist, limited geographic footprint.

Applied didn’t just build data centers. They secured power allocations from utilities eager for local customers to absorb surplus generation. Those allocations took years to negotiate and involved infrastructure commitments from utilities. When Applied locked in 400 megawatts at Ellendale and is scaling to 280 megawatts at Harwood, those aren’t just contracts. Those are utility partnerships where the utility built or dedicated infrastructure specifically to serve those facilities.

You can’t replicate that overnight. The power has to be available. The utility has to be willing. Interconnection has to be approved. Infrastructure has to be built or allocated. In constrained markets that process takes 5-10 years even with unlimited capital. In North Dakota it’s faster, but you’re still talking multi-year timelines to bring significant capacity online.

This is the megawatt land grab thesis. Companies that secured power allocations early created structural advantages that persist regardless of what competitors do later. Applied isn’t just building data centers. They’re locking in power supply enabling AI computing at scale in geography where the economics actually work.

The advantages compound over time. As data centers elsewhere strain grids and drive up costs, North Dakota maintains surplus generation and competitive rates. As cooling costs rise with extreme weather, North Dakota’s climate advantage grows. As transmission constraints bind elsewhere, North Dakota’s local consumption model becomes more attractive. The gap widens.

This isn’t about Applied being better operators. This is about controlling power infrastructure in geography where structural conditions create sustained advantages. Operational excellence matters for execution. But the moat comes from controlling power allocations in a market where power is both abundant and favorably priced due to generation surplus and transmission constraints.

The power infrastructure isn’t just an input. It’s the barrier to entry. And barriers built on physical infrastructure and multi-year utility partnerships don’t erode quickly just because competitors want access.

20251126

You bring a lot of good energy for the stock that is appreciated. I think it will be equally useful if you focus on other side of the coin analyzing objectively their debt situation, note offering, equity offerings and other things so one can see both risk and rewards. Stock price is never random, they represent risk and rewards. The market forces analyze everything. If everything was sunshine, it would already be $50+ you know it. So let’s see what’s your take on debts, note offering, equity offerings and other things that may become challenging, see if you can be objective! Thanks. MNK3240

Fair question. Let me walk through the capital structure and execution risks.

Their debt position has evolved significantly. A year ago in their Q2 FY2025 report, they had roughly $800 million in total debt. The $2.35 billion senior secured notes that closed November 2025 brings current total debt to approximately $3.2 billion. That’s meaningful leverage against a market cap that’s in the $6-7 billion range.

The $450 million convertible notes from November 2024 carry a 2.75% coupon with conversion at $9.75 per share. That’s a 32.5% premium to the $7.36 price when they issued. The capped calls at $14.72 limit dilution at the 100% premium level. The company can’t force conversion before December 2027. Noteholders convert when it’s profitable for them, not when the company decides. If the stock trades below $9.75, they don’t convert. If it trades between $9.75 and $14.72, the capped calls protect against dilution. This is standard infrastructure financing.

The $2.35 billion senior secured notes at 9.25% due 2030 are the real leverage concern. These were issued at 97% of par to fund construction of the 100 MW and 150 MW facilities at Polaris Forge 1. The notes are secured by first-priority liens on APLD Compute’s assets with full subsidiary guarantees. Applied Digital provides completion guarantees, meaning they fund whatever’s needed to finish construction if project financing falls short. That creates direct parent company obligation.

The 9.25% interest rate is the market pricing credit risk. That’s materially higher than the 2.75% on convertibles. On $2.35 billion, annual interest approaches $217 million. Add existing debt service and total annual interest likely exceeds $250 million. Interest expense already jumped 186% year-over-year in Q2 fiscal 2025, from $2.6 million to $7.5 million, and that was before the big notes.

There’s also $150 million in senior secured debt with Macquarie Equipment Capital from November 2024, used to refinance the CIM Group facility. Better structured as project-level financing, but still adds to the burden.

The debt works if they execute. Polaris Forge 1 at 400 MW generates roughly $730 million annual revenue from the CoreWeave contracts. At 47-50% NOI margins, that’s $340-365 million in annual NOI. Polaris Forge 2 adds another $170-180 million in NOI. Combined NOI of $510-545 million covers $250 million in debt service with reasonable margin.

The execution risk is timing. First revenue started late 2025 with 50 MW operational. Full 400 MW won’t be done until construction completes, likely extending into 2026 and beyond. During construction and ramp, they service $250+ million in annual interest while revenue scales from current $60-70 million quarterly toward the $250+ million quarterly needed to support the structure. Construction delays push revenue out. Utilization shortfalls reduce cash generation. Cost overruns trigger completion guarantees requiring equity injections.

The concentration compounds this. CoreWeave represents most of the $11 billion at Polaris Forge 1. One unnamed investment-grade hyperscaler at Polaris Forge 2. If CoreWeave’s business deteriorates, the entire debt structure becomes unsustainable. Customer concentration creates single points of failure.

Beyond the convertibles, they’ve raised equity through various offerings. The Macquarie preferred equity facility gave Macquarie 15% of the HPC business for the $5 billion commitment. That’s dilution even if management frames it as reducing equity needs. Authorized shares increased for convertible conversion capacity, creating overhang.

$3.2 billion debt against $6-7 billion market cap puts debt-to-market-cap over 50%. For pre-revenue infrastructure assets still in construction, that’s aggressive. The debt works once cash flows materialize. Until then, they operate with significant leverage during the period when execution risk is highest.

You’re right that if everything was certain, it would already be priced in. The market is pricing execution risk around construction timelines, utilization ramp, customer concentration, and servicing debt during the transition from construction to operations. The stock declines alongside everything AI-adjacent despite contracted revenue. That’s not pure sector rotation. That’s concerns about leverage and execution showing up in price action.

What could go wrong layers capital structure on top of operational execution. Utilization ramps slower, pushing break-even out and requiring more capital. Construction faces delays or overruns, triggering completion guarantees and forcing dilutive equity raises. CoreWeave or the second hyperscaler face business challenges impacting contract fulfillment. Hyperscalers accelerate vertical integration, reducing third-party capacity demand. The company needs more capital before cash flows cover debt service, bringing more dilution.

Large infrastructure projects run over budget and behind schedule. Any delays push revenue out while interest accrues. The $250+ million annual interest creates a breakeven point that’s higher than a lightly leveraged competitor, reducing margin for error.

The risks are real. The leverage is real. The execution risk is real. The concentration risk is material. This isn’t risk-free infrastructure with contracted cash flows eliminating uncertainty. This is a leveraged bet that management executes construction on time, customers fulfill contracts, utilization ramps as modeled, and nothing major disrupts the business during the 12-24 months transitioning from construction to cash generation.

My view is the contracted revenue, secured power allocations, and utility partnerships create structural moats justifying the execution risk at current valuations. The institutions who underwrote $2.35 billion in senior notes and Macquarie’s $5 billion facility did extensive diligence and believe contracted cash flows support the debt. NVIDIA put in $160 million. These aren’t gambling. They underwrote the cash flows and assessed the risks as acceptable.

I’m not a blanket bull on everything AI-adjacent. I’m incredibly bearish on quantum computing stocks like QBTS, RGTI, IONQ, and QUBT. These companies trade at absurd valuations with minimal revenue, zero operational quantum computers solving real problems, and timelines to commercialization that stretch into the 2030s. RGTI trades at over 1,000x forward sales on revenue that doesn’t exist yet. The sector is pure speculation trading on narrative with no falsification mechanism until 2030 or later. Same goes for nuclear startups like OKLO, SMR, and NNE. OKLO has a market cap around $15 billion with zero operational reactors, zero revenue, and a regulatory rejection from the NRC in 2022. They’re selling a future that requires solving fuel supply chains, regulatory approval, and technical challenges that traditional nuclear couldn’t crack in decades. These aren’t infrastructure plays. They’re lottery tickets.

APLD is different because they have contracted revenue with investment-grade counterparties, operational facilities coming online now, and power allocations that create structural moats. The thesis is falsifiable quarterly as revenue ramps and utilization proves out. The risks are execution and leverage, not whether the business model works in theory. That’s an asymmetric bet I’m willing to take. Quantum and nuclear startups are asymmetric the other direction. Unlimited downside, theoretical upside that may never materialize.

I’m betting APLD executes. The debt works if they hit targets. The dilution is justified if the power allocations create the moats I think they do. But I’m not pretending the stock goes straight up or that there’s no risk. The market is pricing meaningful execution risk, and that’s appropriate given the leverage and timeline. If you think execution risk is higher than I do, or you don’t believe contracted revenue justifies current valuation with this debt load, that’s a coherent bear case. I disagree, but these are legitimate concerns worth weighing before taking or holding a position.

20251130

The next earnings report, expected mid-to-late January, is the one I’ve been waiting for since I began building my long position.

I know I’m getting slightly ahead of myself here. It’s still about two months away. But I’m genuinely eager for this one in a way that has nothing to do with typical earnings anticipation. This isn’t about beating analyst estimates or raising guidance. This is the quarter where contracted revenue starts converting into recognized revenue on financial statements. This is where the investment framework either proves itself or doesn’t.

Phase I at Polaris Forge 1 went live in October. Phase II hit Ready for Service November 24th. That’s 100MW operational, contracted to CoreWeave. Q2 fiscal 2026 covers September through November, which means this quarter captures the first revenue recognition from live capacity. Phase I operated through October and November. Phase II came online late in the quarter, giving us roughly a week of full 100MW operations. So we’re not seeing a complete quarter of revenue yet, but we’re seeing it start.

That’s what matters. The shift from future tense to present tense.

For months, the conversation has been about approximately $16 billion in total contracted revenue across both campuses. The market’s response has been consistent skepticism. “Sure, contracted. Let’s see it actually generate cash.” And that’s fair. Contracted revenue is a promise. Revenue recognition is proof. The gap between those two is where execution risk lives, where unit economics get tested, where models meet reality.

Next earnings is when that gap starts closing.

We’re about to get actual numbers. Revenue per megawatt. Operating margins on live capacity. Proof that capacity coming online generates the economics the thesis predicts. No more extrapolating from guidance. No more trusting that the math works when facilities go live. Just financial statements showing what happens when contracted capacity starts operating and generating cash.

This is the data point everything has been building toward. The entire power allocation thesis rests on infrastructure operators generating strong economics from secured capacity and hyperscaler contracts. We’ve had the operational updates, the construction milestones, the capacity announcements. Now we get to see what those translate to financially.

Q3 will show the first full quarter of 100MW operations. That’s when the revenue run rate becomes clear. But Q2 is where it begins. Where “this will generate revenue” becomes “this is generating revenue.” Where the thesis stops being theoretical and starts being measurable.

The market has been selling these stocks on sentiment while the underlying business involves contracted cash flows. Everything AI-adjacent moves together regardless of whether companies have signed contracts or speculative promises. Revenue recognition breaks that pattern. It gives the market concrete data to value instead of projections. The economics either support the investment case or they don’t. The margins either validate the framework or they don’t. We’re about to find out.

If the numbers validate what the thesis predicts, the conversation shifts entirely. It stops being “can they execute?” and becomes “what do the unit economics look like as more capacity comes online?” It stops being “do these contracts generate cash?” and becomes “how does this scale across the remaining buildout?” Revenue recognition forces the market to price based on demonstrated economics rather than sentiment about AI infrastructure as a category.

I’ve watched the facilities get built. Watched Phase I go live, then Phase II, both on communicated timelines. But none of that shows up in market pricing until it appears in financial statements. The market doesn’t care about operational milestones until they convert to revenue and margins. That’s the gap I’m waiting to close.

This is just the beginning. Just 100MW starting to show up in reported revenue. More capacity comes online over time as the campus expands. But you have to start somewhere. Q2 is where it starts. Where contracted revenue begins proving itself on income statements. Where the framework gets tested against actual results.

That’s why I’m eager. That’s why this earnings matters more than any that came before it. Two months away, and I’m already counting down.

20251211

Amazon will spend over $125 billion on AI infrastructure this year and has already said 2026 will be higher. Microsoft spent $88 billion in fiscal 2025 and confirmed fiscal 2026 will accelerate further. Alphabet raised guidance to $93 billion and signaled a “significant increase” for 2026. Meta is at $72 billion and climbing toward $100 billion. That’s over $400 billion from just four companies in 2025, with each projecting higher for 2026. Add Blackstone’s $70 billion in data center assets and $100 billion pipeline. Add the $500 billion Stargate commitment from OpenAI, SoftBank, and Oracle.

The skeptics look at these numbers and see leverage building toward collapse. They’re not wrong that the debt is historic. They’re wrong about what kind of debt it is.

Start with where the money goes. Amazon commits $125 billion in AI capex. That capital flows to NVIDIA, who deposits in the same banks that provide Amazon’s credit facilities. It flows to data center operators financed by Blackstone and Macquarie, institutions raising capital from pension systems. It flows to utilities issuing bonds purchased by the fixed income arms of those same asset managers. It flows to construction firms whose workers deposit paychecks that become liquidity for additional infrastructure lending.

The money doesn’t leave the ecosystem. It cycles through the same institutional hands.

This isn’t leverage building toward a Minsky moment. It’s velocity in a closed system where the major participants are lender, borrower, and customer simultaneously.

Trace a single pension fund’s exposure. They own Microsoft stock directly. They hold shares in a Blackstone infrastructure fund financing data center operators. They own utility bonds powering those data centers. They hold equity in banks providing credit facilities to hyperscalers. They hold NVIDIA in their growth allocation.

Their returns depend on every layer executing.

This sounds like diversification. It’s actually concentration in a single thesis wearing different clothes. If AI infrastructure fails, they don’t lose on one position. They lose everywhere simultaneously.

That exposure changes behavior.

When a bank has financed a data center operator, holds equity in the hyperscaler tenant, and manages pension assets invested in both, the incentive is to extend additional credit rather than trigger default. Forcing bankruptcy impairs the loans, damages the tenant relationship, and creates losses that flow back to the bank’s own asset management clients.

When an asset manager has deployed capital across multiple layers of the same value chain, marking down one position damages the others. The correlation is too tight. Better to maintain valuations and wait for contracted cash flows than trigger a writedown cascade.

When a pension fund’s returns depend on every layer performing, forced liquidation damages the entire chain their beneficiaries rely on.

The rational response at every node is continued cooperation. Defection costs more than continuation.

The structure resembles sovereign debt more than corporate speculation. When Japan issues debt to domestic institutions, default becomes nearly impossible because the same actors would harm themselves. The central bank, commercial banks, and domestic asset managers are locked into mutual dependency. None can defect without damaging their own position.

AI infrastructure financing has developed similar characteristics. JPMorgan finances Amazon’s buildout. Amazon pays NVIDIA. NVIDIA deposits at JPMorgan. Unwinding any piece damages all the others.

This is what the bubble framework misses. Bubbles pop when marginal buyers disappear, revealing nothing underneath. The AI buildout doesn’t depend on marginal buyers. It depends on committed capital from institutions whose existing exposure makes continued commitment rational regardless of sentiment. The question isn’t whether new money arrives. It’s whether existing money defects from positions where defection means accepting losses across every layer simultaneously.

No one has that incentive. Everyone has the opposite incentive.

The skeptics see half a trillion in annual hyperscaler capex and assume fragility. They’re applying a framework designed for leveraged speculation to a structure designed for mutual dependency. The debt isn’t sitting on balance sheets waiting to explode. It’s circulating through a closed system where the participants have already decided the buildout will continue because they can’t afford for it not to.

That’s not fragility. That’s lock-in.

@Wride

Really wonderful description of the closed loop and the incentive structure — I’m still thinking about it.One framing I keep coming back to is that the loop feels more like a bridge than a foundation. It can sustain the buildout and smooth volatility, but the system’s long-run solvency still seems to hinge on whether AI generates real, external cash flows for the companies actually implementing it.

And then whether hyperscalers are able to capture a meaningful share of that value. I’m not sure that’s guaranteed — intelligence may ultimately behave more like a commodity than a rent-bearing asset.

One other nuance I’ve been wrestling with: I wonder if the argument gives banks and large institutions a bit too much credit for coordination. Between regulatory “Chinese walls,” internal turf wars, and independent P&Ls, they often feel less like unified machines and more like loosely coupled (sometimes warring) teams.

Curious how you think about those pieces.

The bridge framing is right, and I should be clearer about what I think it’s bridging to. Not speculative future revenue – contracted future revenue that just hasn’t been collected yet. The data center operators have signed 15-year leases with hyperscalers. The cash flows aren’t hypothetical. They’re scheduled. The bridge needs to hold until the facilities come online and start generating against those contracts, not until AI “proves out” in some broader sense.

Your commoditization point is the real bear case, but I’d push back on where the risk sits. If intelligence commoditizes and hyperscalers can’t capture rent, that’s Microsoft’s problem. The data center operator still has a 15-year lease. The utility still sells power. The pension fund’s infrastructure position still throws off contracted returns. The commoditization risk is upstream from where I’m positioned. I’m not betting on hyperscalers capturing AI value. I’m betting on them needing physical infrastructure regardless of whether they capture it.

On bank coordination, I think you’re right that I’m not describing active coordination. I’m describing aligned incentives producing similar behavior independently. JPMorgan’s infrastructure lending desk doesn’t call their asset management arm to strategize. They both independently calculate that extending credit beats triggering default because both units’ returns depend on the same underlying buildout succeeding. The outcome looks like coordination but it’s emergent. No room required.

20251211

Triple digits or thesis failure. That is my exit strategy. There is no stop loss. There is no “taking profits to derisk.” There is holding until the thesis plays out or holding until I’m forced to admit I was wrong about everything, at which point I will gaslight myself into forgetting I ever owned it. That’s the downside scenario. I’ve made peace with it.

People ask when I’m selling. When the contracts evaporate? When the hyperscalers collectively decide AI was a bad idea and pivot back to whatever they were doing before? When Wes stops executing? I’ve watched him operate. I’ve watched him secure contracts the market still hasn’t fully priced in. The man is on his way to becoming a billionaire and I’d like to be in the seat when he gets there. That’s not a sell trigger. That’s a reason to hold tighter.

My broker thinks I need an exit plan. I have one. It’s called triple digits. He means a trailing stop or a target price where I “lock in gains.” I mean I’m not leaving until I’ve extracted everything this position owes me. We’re having different conversations. He gets paid when I transact. I get paid when I don’t. Misaligned incentives. I’ll take my advice from the guy building the company, not the guy building a commission.

A binary exit strategy means I don’t check the stock every day wondering if today’s the day. I don’t calculate whether I’ve made “enough.” I don’t negotiate with myself about what counts as a win. The thesis plays out or it doesn’t. I get paid or I learn an expensive lesson. Simple. Clean. No room for self-sabotage.

Triple digits or thesis failure. Everything else is just the market trying to shake me out. And I don’t shake.

The End

17% drop 20251215

kavastock:

The price action today makes visible who sized correctly and who didn’t.

You can tell from the posts. The ones who sized for volatility are annoyed but functional, talking about the thesis, making decisions from relative calm. The ones who over-leveraged are somewhere else entirely. Panic in the syntax. The stomach-ache showing through the screen.

I empathize with them. I’ve been there. You believe in the thesis so strongly that conservative sizing feels like a failure of conviction. So you size up. And it feels fine on green days. Then a day like today happens, and the leverage becomes the only thing you can feel.

The lesson is always the same: size for the volatility you’re going to experience, not the volatility you hope to avoid. If a near 20% drawdown makes you unable to think clearly, you’re too big. The position size that lets you observe a red day with disappointment rather than dread is the correct size.

One can only talk so much about it. The advice is everywhere. Everyone nods. Then conviction combines with greed and the sizing creeps up anyway. The lesson doesn’t land until the pain teaches it directly.

C’est la vie.

I know this is stressful to many. These sequences are never fun to sit through, regardless of conviction or timeframe. Watching a position bleed day after day activates every system in your brain designed to make you act, and acting is usually the wrong response. So let me try to explain what’s actually happening beneath the price action.

What you’re watching looks like chaos. It isn’t.

This is the mechanical process of institutional repositioning, and it has a logic that becomes visible once you understand who’s doing what and why.

Large funds can’t exit or enter positions the way retail does. A fund managing billions that wants to build a position in a $6.4 billion market cap name can’t just buy. The order would move the price against them before they filled a fraction of their target. So they accumulate slowly, ideally while price is falling, buying into weakness rather than chasing strength. The optimal accumulation environment is exactly what you’re seeing: falling prices, negative sentiment, retail capitulation.

The corollary is also true. When funds want to distribute, they need buyers. The optimal distribution environment is rising prices, positive sentiment, retail enthusiasm. They sell into strength.

This creates a structural inversion. The price action that feels worst for retail, the relentless bleeding that shakes conviction, is often the price action that precedes institutional accumulation. The price action that feels best, the rip that validates the thesis, is often distribution.

The mechanism underneath today’s action has a few components.

Short sellers are pressing. APLD carries roughly 34% short interest, and the playbook is familiar: pressure the stock into technical breakdowns, trigger stop losses, create the narrative of failure that justifies more shorting. This is self-reinforcing until it isn’t. Shorts eventually cover, and when they do, they’re buying.

Tax loss harvesting is seasonal. December brings forced selling from funds that need to realize losses before year end. This selling is indifferent to thesis. It’s accounting, not analysis. The fund isn’t saying the stock is worth less. It’s saying they need the loss on this year’s books.

Liquidity algorithms are hunting. The stops clustered at obvious technical levels are visible to anyone with order flow data. Running those stops, triggering that selling, creates liquidity for larger players to accumulate. The retail trader who gets stopped out at the low is often providing shares to the institution that will hold them into the next leg up.

None of this is conspiracy. It’s just mechanics. Large players have constraints retail doesn’t have. Those constraints create predictable behaviors. The behaviors create patterns that look like manipulation but are really just the physics of how size moves through markets.

The question for anyone holding through this: are you watching signal or noise? The institutional mechanics are noise. Sophisticated, structured, painful noise, but noise. The signal is in the filings, the contracts, the megawatts. Price will eventually reflect fundamentals. Between now and eventually is the volatility you sized for.

kavastocks

The equilibrium zone is being tested again. The rally from late November failed at resistance, and price has returned to the $22-23 level that needs to hold for the structure to remain constructive.

Price pushed from the low $20.00s to $30+ in early December, exactly as the prior analysis anticipated. But it couldn’t clear the overhead resistance. The CHoCH marker around $30 that was reclaimed as support failed to hold, and price has since given back the entire rally. Currently price sits just above S1 ($22.13) and right at the equilibrium zone. This is the same level that caught the November low. The market is asking the same question twice: is there a bid here?

The Ichimoku cloud frames the failure. Price pushed into the cloud, spent time in transitional territory, and rejected. It never reached the upper boundary near $39-40 where the October highs printed. The cloud overhead remains uncleared resistance. Price is now back below the cloud entirely, which shifts structure from transitional back to corrective. Below the cloud means sellers remain in control until proven otherwise.

The volume profile shows why this zone matters. The $22-23 area represents an important volume node of the range. This is where a good amount of positioning has occurred. That concentration works both ways: it can act as support because there’s a wall of buyers who accumulated there, or it can act as a magnet that keeps pulling price back. Right now it’s doing both.

The weak high right below R4 $40.02 marked on the chart tells the story. October’s high was the structural peak. Every rally since has printed a lower high. The December push to $30+ was another lower high. Until price reclaims $40 and holds it, the sequence of lower highs remains intact.

Risk management still keys off this equilibrium zone. A sustained break below $22 changes the character from “corrective within an uptrend” to “downtrend until proven otherwise.” The S2 level at $18.85 becomes the next logical target if this zone fails. Conversely, holding here and building a base would set up another attempt at the resistance overhead.

The structure has deteriorated from constructive back to corrective. Momentum that confirmed the turn in early December has reset. The equilibrium zone held once. Now it needs to hold again. The burden of proof is on buyers to defend this level and rebuild the structure that just broke down.

kavastocks

In a market full of scumbag CEOs, we’re lucky to have Wes.

That sounds like cheerleading until you compare him to the norm. Most CEOs in this space treat shareholders as a funding source, not a constituency. They dilute without warning, overpromise on timelines, go quiet when things get hard, and resurface when they need another raise. The incentives push toward hype because hype sells stock and stock funds operations.

Wes operates differently. He communicates when there’s news and when there isn’t. He’s been clear about the vision from the start: secure power, build infrastructure, sign long-term contracts, execute. No pivots to whatever narrative is hot that quarter. No chasing shiny objects. When the senior secured notes dropped and the stock sold off, he didn’t panic or start making excuses. He stuck to the plan because the plan was already working.

A CEO who thinks in years instead of quarters, who treats retail shareholders like they deserve real information, who builds a company instead of a stock promotion, that’s actually rare. Especially in small caps where the temptation to play games is highest.

It’s difficult to notice good leadership until you’ve been burned by bad leadership. Once you have, you recognize what Wes is doing and why it matters.

Applied Digital (APLD) shares last traded at $24.52, up 1.8% from their previous close, before U.S. markets shut for the New Year’s Day holiday. Shares traded between $23.97 and $25.93 in Wednesday’s session.

The small-cap data-center builder has become a volatile proxy for spending on AI infrastructure, where power availability and access to advanced chips can dictate who gets capacity and when. Investors are focusing on whether Applied Digital can translate that demand into funded projects and recurring cash flow.

Applied Digital said on Dec. 29 it entered a non-binding term sheet — a preliminary outline of a deal — to spin out its Applied Digital Cloud business and combine it with Nasdaq-listed Ekso Bionics to form ChronoScale. Applied Digital would own about 97% of the combined company, which the firms expect to close in the first half of 2026, subject to approvals. The company said the cloud unit deployed Nvidia’s H100 graphics processing units (GPUs) at scale in 2023 and generated about $75.2 million in revenue in the 12 months ended Aug. 31, 2025. Applied Digital Corporation

Northland named Applied Digital its “Top Pick for 2026” and kept an Outperform rating with a $40 price target. The firm pointed to demand for power from hyperscalers — large cloud companies that buy data-center capacity in huge blocks — and to Applied Digital’s execution and development pipeline, alongside a medium-term REIT plan. A real estate investment trust (REIT) is a tax-advantaged structure often used to hold income-producing property. TipRanks

Lake Street analyst Rob Brown reiterated a Buy rating and raised his target to $45, saying a spin-out could help surface the value of the cloud GPU operation. He called it “largely a forgotten asset within Applied” and said the business is operating six GPU clusters and generating about $75 million in annual revenue. TipRanks